Lower or Eliminate Your Medi-Cal Share of Cost

Which Best Describes Your Situation?

- I already know my monthly Share of Cost and the amount of premium I need to get it to Zero.

- Scroll down for plans on dental, vision and Medi Gap – premiums to lower your share of cost to Zero.

- I do not know the correct Share of cost or premium needed

- Use our Medi-Cal Share of Cost Calculator as a preliminary estimate. Compare the result with your county Notice of Action or the amount supplied by your county worker.

- I need more information on what share of cost is, why or if buying insurance is a real legitimate way to lower share of cost.

- Aged & Disabled and Medically Needy Medi-Cal Programs Canhr 7/20/2026

- How to eliminate the Medi-Cal Share of Cost to get full Medi-Cal coverage Center for Health Care Rights SHIP 4/2025

- How Can I Avoid a Medi-Cal Share of Cost? You Tube Attorney Video

- Are You a Family Member or IHSS Caregiver?

- Often, the person researching Medi-Cal Share of Cost is not the person receiving care—it is a **son, daughter, other family member, or IHSS caregiver** trying to help.

-

If the person you care for has a Medi-Cal Share of Cost, that amount can also affect **how you are paid for IHSS services**. The recipient may be responsible for paying part of your authorized IHSS wages directly before the State pays the balance.

-

If an allowable health, dental, or other insurance premium is reported to Medi-Cal and **Medi-Cal reduces or eliminates the Share of Cost**, the practical result can be important for the caregiver: instead of having to collect that Share of Cost portion from the person you care for, **the State can pay the authorized IHSS wages that are no longer subject to the Share of Cost.**

-

So reducing a Share of Cost may help **both the person receiving care and the person providing it**.

Step 2 — Select the Monthly Premium Shown by the Calculator

y

How much insurance premium do you need to reduce your Share of Cost to $0?

- $1–$84 per month:

Get quotes and enroll dental or vision plan

. - $85–$425 per month: Complete the AmFirst Maximum Care Application after checking with Steve. AmFirst offers premium choices within from $85 to $425

- Applications are often processed quickly, and proof of coverage can usually be provided within 24 hours after approval. Then you can easily upload (instructions) to BenefitsCal.com

- Just complete the one page application and email [email protected] to us.

- $426–$600 per month:

- A combination of the AmFirst Maximum Care application

- and another qualifying dental or vision premium

- $601 or more: The situation should be reviewed individually before applying. Send us the information below

-

- Medi-Gap premiums

- The monthly Share of Cost shown by your county.

- Your county and ZIP code.

- Whether you have Medicare Parts A and B and the premium amounts

- Any premiums you already pay for Medicare Part B, Part D, Medicare Advantage, Medi-Gap, dental or vision.

- Whether the problem concerns future months or previous months.

- Your Notice of Action from the county

- Email Steve Your Share of Cost Information

- Our email is encrypted by PauBox

After Enrollment:

Send Proof to the County

After approved enrollment, the county may request a proof-of-coverage letter, premium invoice, effective date and evidence that the premium was paid. Keep copies of everything submitted and follow up with your county worker.

See the complete proof and BenefitsCal document-upload instructions

.

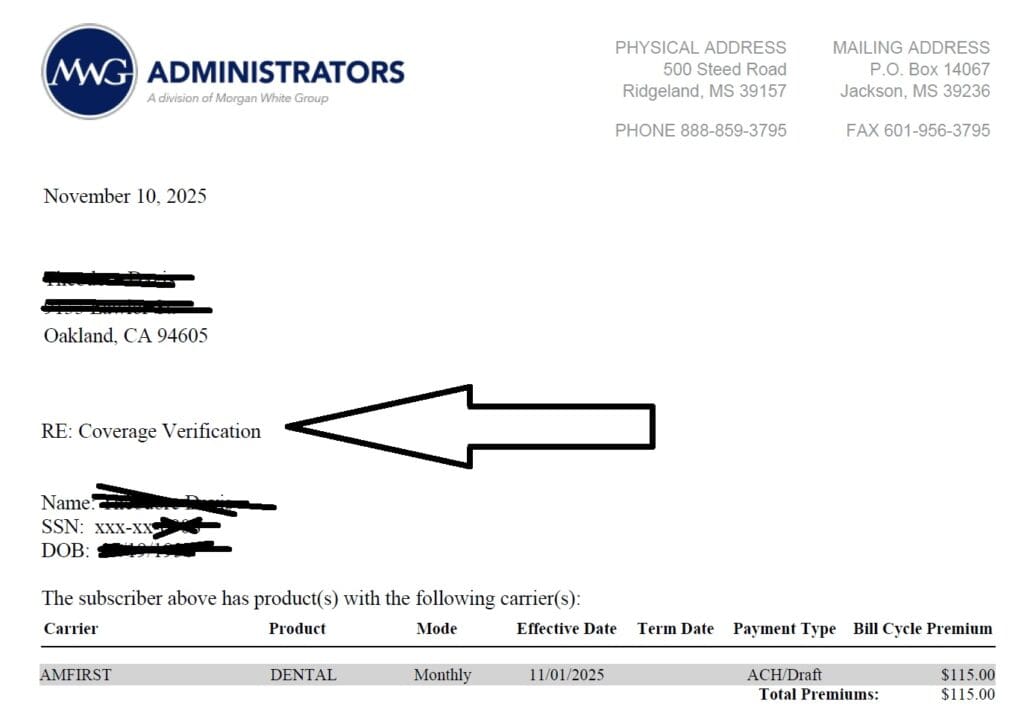

Sample Proof of Dental Insurance for BenefitsCal

Share of Cost Testimonials

- “Medi-Cal reviewed my Mom’s case and eliminated her Share of Cost effective February 1. My family is very grateful that this issue was resolved in a very timely manner.” — Don V.

- “Eliminating her Share of Cost will allow her to stay living at our home longer, so it’s very wonderful.” — Mary

- “You are a wealth of knowledge, and I am so grateful to connect with you.” — Carie C.

- See additional Share of Cost comments and testimonials.

- See general client testimonials

- See this Reddit discussion about Share of Cost

Steve Shorr has specialized in California health insurance since 1975. There is no separate charge for assistance with an insurance application. Compensation is paid by the insurance company when applicable. Steve is an insurance agent, not a county eligibility worker, attorney or tax adviser.

Child Sub Pages

This page provides general educational and insurance information. Medi-Cal eligibility and Share of Cost decisions are made by the county based on the individual facts and current program rules.

References & Citations

- California Medi-Cal rules provide for the deduction of health-insurance premiums in applicable Medically Needy income calculations.

- See California Code of Regulations, Title 22, §50555.2

- See the DHCS Non-MAGI Medi-Cal Guide

- Center for Health Care Rights Plain English How to Eliminated Share of Cost

- CANHR Fact Sheet on Share of Cost

- Your county eligibility worker makes the final determination for your individual case.

- See California Code of Regulations, Title 22, §50555.2

Resources & Links

- Worksheets for Determining Eligibility Under the Aged & Disabled Federal Poverty Level (A&D FPL) Medi-Cal Program Disability Rights CA

- CHCF explanation SOC Share of Cost Rev December 2017

- Includes cost calculation worksheets

- Chapter 2 – DETERMINATION OF MEDI-CAL ELIGIBILITY AND SHARE OF COST

- Medically #Needy Program (CANHR Fact Sheet 8.14.2023) (My highlighted version)

- Western Poverty Law *

- CA Health Care Advocates * Read the full article from CHCF *

- AB 715 Fact Sheet *

- CHCF for 3 other examples!

- CHFC explanation of Share of Cost

- Legal Aid of San Mateo is your Share of Cost Calculated Correctly

- CA Code of Regulations Article 10 Income

-

Resources & Links

eva lovia naked

simsons porn

kpop demon hunters sex

https://www.laaconline.org/laacmembers/

member roster of legal aids in CA!!!

https://ridleylawoffices.com/guides/medi-cal-share-of-cost-california/

(805) 244-5291

[email protected]

https://www.caregiveroc.org/

714.446.5030

https://www.inlandlegal.org/

Senior Line (800) 977-4257

https://www.ocelderlaw.com/medi-cal-share-of-cost-calculator

(714) 525-4600

https://www.reddit.com/r/IHSS/comments/1socie0/share_of_cost/

ShareofCost.com 910 W Lomita Blvd Suite #E PO Box 910 Harbor City California 90710-0910 Office: 310-534-3444

https://dennisfordhamlaw.com/paying-for-necessary-medical-expenses-with-medi-cal-share-of-cost/

707.263.3235

https://pasadenalawgroup.com/understanding-share-of-cost-in-californias-medi-cal-program/

https://pascc.org/understanding-ihss-share-of-cost/

(408) 350-3206 | [email protected]

https://www.udw.org/uncategorized/share-of-cost-out-of-pocket/

1-800-621-5016

https://www.eldercarelawca.com/medi-cal-share-of-cost/

Address:

475 Washington Blvd, Suite 200, Marina Del Rey, CA 90292

Phone:

(866) 822-7211

Email:

[email protected]

https://www.carehomefinders.com/contact

(800) 330-5993

Our Email: [email protected]

https://pascla.org/understanding-share-of-cost/

Legal Aid Foundation at 213-640-3926

Contact Us By Phone

Toll Free: 877-565-4477

Fax: 818-206-8000

TTY: 626-737-7512

Contact Us

[email protected]

https://www.laaconline.org/

(510) 893-3000

[email protected]

I appreciate your guidance on getting to zero share of cost, very informative! 🌟

Thank you for your help – I’ve spent years trying to figure this out and I’m glad you were able to help me.

Hi Steve,

Thank you for the nice presentation, [Loom explanation of an email] very helpful to see everything onscreen.

Best regards,

Leslie

Hi Steve,

Our zoom meeting this morning was very much appreciated.

I really benefited a lot from our discussion

Thank you very much for your assistance.

Sincerely,

Don V