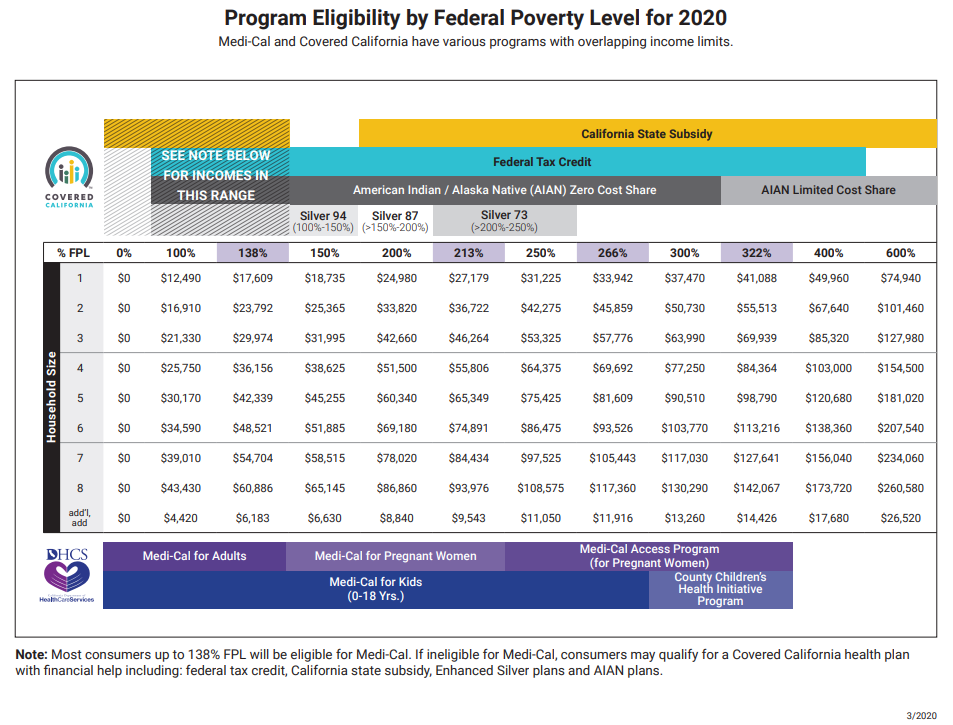

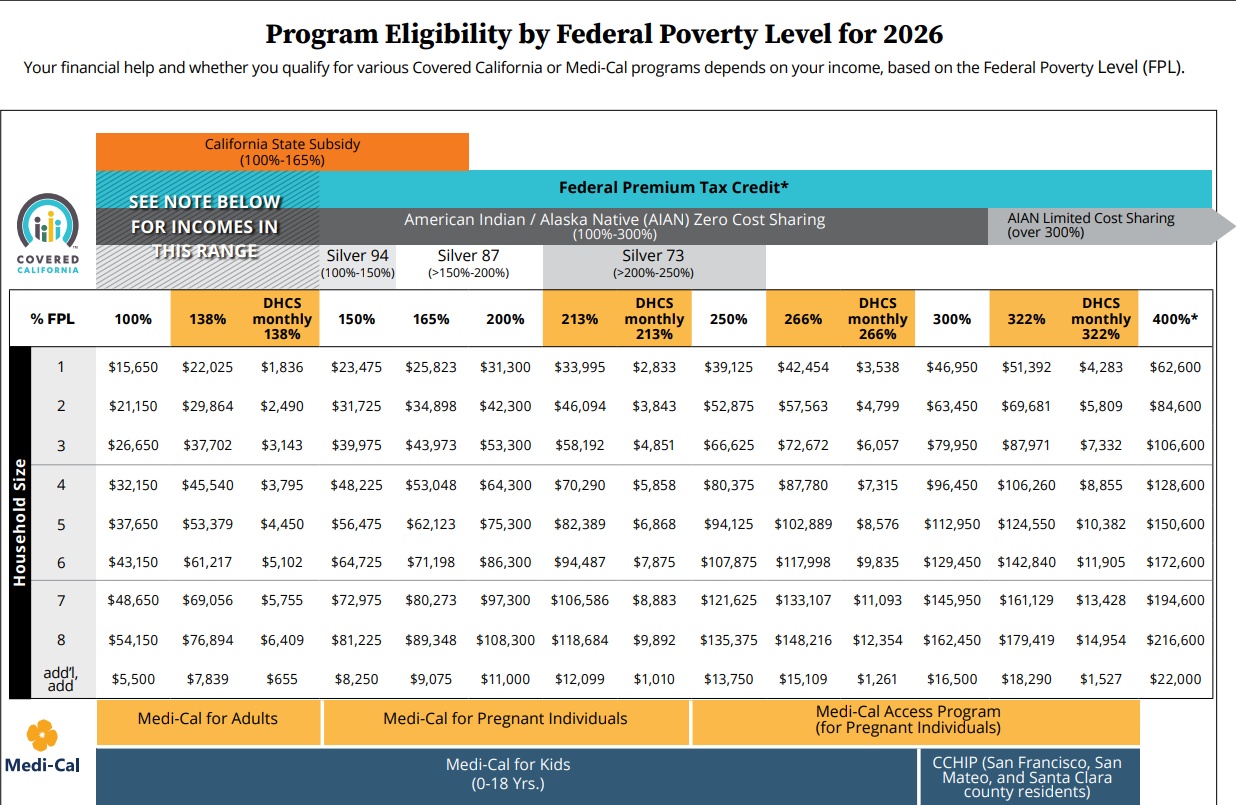

Covered California Income Chart 2026

Do you qualify for Medi-Cal, Covered California subsidies, or an Enhanced Silver plan?

If you are trying to figure out whether your income is too low, too high, or just right for Covered California… this page will give you a quick starting point.

The key: your eligibility is usually based on your projected yearly MAGI income and your household size.

And you do not have to figure this out alone.

I am a Covered California Certified Insurance Agent, and there is no extra charge for my help when you use me as your agent.

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

Quick Answer

Here is the short version:

Up to about 138% FPL → Medi-Cal

100% to 400% FPL → Covered California subsidies

Up to 250% FPL → Enhanced Silver (lower deductibles and copays)

100% to 165% FPL → Extra California subsidy (2026)

Important: These are general guidelines. Final eligibility depends on your full application, ZIP code, ages, and whether you qualify for Medi-Cal.

Before You Use the Chart

Most people make one of two mistakes.

Mistake #1: Using the wrong household size

Mistake #2: Using last year’s income instead of this year’s estimate

Covered California usually uses your projected yearly MAGI.

If your estimate is off, your subsidy may be adjusted later when you file your taxes.

How to Use This Page

Step 1: Determine your household size

Step 2: Estimate your yearly MAGI income

Step 3: Compare your income to the chart

Step 4: Identify whether you may fall into Medi-Cal, subsidy, or Enhanced Silver range

Step 5: Confirm it with a real quote

Having Trouble Reading the Chart?

You are not alone.

If the chart looks small, blurry, or confusing on your phone, skip the guesswork.

Just email me:

- Your ZIP code

- Your household size

- Your date of births

- Your estimated yearly MAGI income

Email: [email protected]

I will help you figure out your next step.

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

What Counts as Income (MAGI)?

MAGI usually starts with your Adjusted Gross Income.

Then, depending on your situation, you may add:

- Non-taxable Social Security

- Tax-exempt interest

- Foreign income

The important part: Covered California usually looks at your best estimate for the upcoming year, not just last year.

Frequently Asked Questions

Is Covered California based on monthly or yearly income?

Usually yearly projected income. Medi-Cal can work differently.

What if my income is too low?

You may qualify for Medi-Cal.

What if my income is too high?

You can still buy coverage, but without subsidies. If you want Silver, it may be less if we go direct and not through Covered CA

What if my income changes?

You should report it. Otherwise your subsidy may be too high or too low at tax time.

Do I have to figure this out myself?

No. I can help at no additional cost.

Need Help?

If you want help figuring out your eligibility, just reach out.

Steve Shorr

Covered California Certified Insurance Agent

Email: [email protected]

| Check Federal Poverty Level, Subsidy & Quote | Email Steve | Schedule Zoom |

This is general information only and not tax or legal advice. Final eligibility is determined by official program rules and your application.

Nov 7, 2025 Summary of video below

Covered CA still offers the original subsidies. Check out the chart and see if you’re between 138 and 400% the minimum not to be in Medi Cal and the Maximum to get subsidies. If over 400% of course you can still buy coverage!

Compare Health, Dental & Medi Gap Plans including subsidy & Enroll Quotit.net

Independent licensed agent. No obligation.

![]()

Covered CA Certified Insurance Agent

Get Covered CA quotes and Direct Quotes too

Review of the MAGI Medi-Cal income limits for adults and children for 2026. The higher income limits will be updated in the Covered California income table in February.

#FAQ ‘s, Explanations & More Details

Footnotes

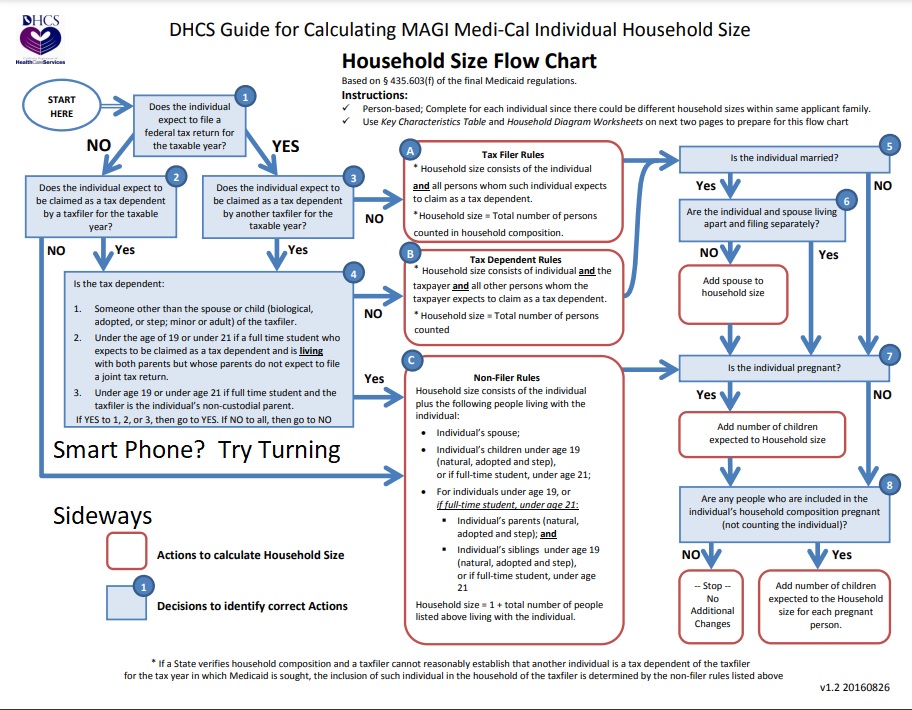

1 What is my Medi Cal or Covered CA Household Size– Definition

Try this Flow Chart for a simpler explanation

How many dependents are on your Tax Return? Section 151

Household Income includes all dependents on your return

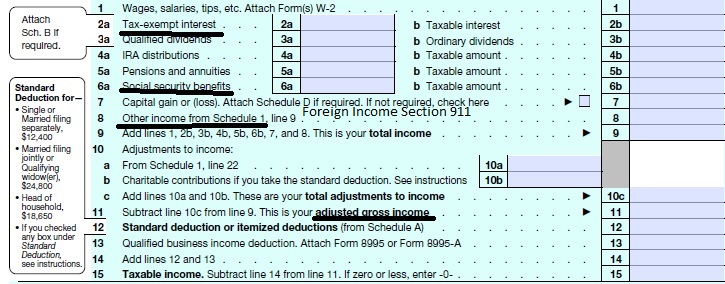

2 What is MAGI Modified Adjusted Gross Income – Line 11 AGI + Social Security, Tax Exempt Interest & Foreign Income

Tax Return Reconciliation of Subsidy is on 8962 at the end of the year

- 4 MAGI based Medi-Cal One can get FREE Medi-Cal base on MAGI Income Line 37 of your 1040 – If your income falls below 138% of the CA Poverty Line on the chart above. There is no longer an asset test, nor estate recovery.

- Medi-Cal versus Covered California Income, Who Decides? Kevin Knauss

- Why Your Covered California Health Insurance Subsidy Dramatically Drops with an Income Increase InsureMeKevin.com

- Getting out of Medi Cal when your income increases?

- If you’re on SSI you should automatically get Medi Cal

- Learn more about Share of Cost Medi Cal and not having to pay extra for IHSS In Home Supportive Services

- If your income is below 138% and you don’t like Medi Cal, you can buy Covered CA or direct, but without subsidies Learn More

5 MAGI Medi-Cal for Pregnant Women

6 Medi-Cal Access Program If you’re pregnant – up to 322% of FPL – Formerly AIM

7 C-CHIP County Children’s Health Initiative Program in three northern CA counties

8 Kids under 19 go in Medi-Cal if MAGI Income is below 266% of Federal Poverty Level. While you can purchase coverage direct from an Insurance Company at Open or Special Enrollment, there is no PTC subsidy or premium tax credit.

Learn More ==> Western Poverty Page 72

9 Enhanced Silver – Cost Sharing 94, 87 & 73 – in addition to subsidies, you get lower deductibles & Co Pays. 94 is better than platinum which is 90 and 87 is better than gold which is 80 – metal level.

Silver 70 has a $2,500 Deductible and Standard Metal Levels, Bronze $5k deductible, Gold and Platinum $0 Deductible

10 Federal Poverty Level FPL My Coverage Plan.com – Definition

FPL gets adjusted annually, IMHO the best way to calculate is to Click here to calculate your premium assistance and get proposals

Federal Poverty Level (FPL): “An income level based on the official poverty line as defined by the federal Office of Management and Budget and revised annually or at any shorter interval that the Secretary of Health and Human Services deems feasible and desirable.” 22 CCR § 50041.5; see also 10 CCR § 6410

Subsidies now go to 600% CA Health Line * But the Big Beautiful bill didn’t renew them?

Why Your Covered California Health Insurance Subsidy Dramatically Drops with an Income Increase Kevin Knauss

11 Use our free calculator to see how much subsidy and enhanced silver benefit you might qualify for. Less than 138% of FPL generally qualifies one for Medi-Cal.

Silver 94 – Under 138% Only if you can’t get Medi-Cal

12 Silver 94 – Under 138% Only if you can’t get Medi-Cal

13 Click here to calculate your premium assistance and get proposals

We are paid by Covered CA and the Insurance Companies to help you, when you appoint us as your agent NO CHARGE!

All our Health plans are Guaranteed Issue with No Pre X Clause

Instant Quote & Subsidy #Calculation

There is No charge for our complementary services, we are paid by the Insurance Company.

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- We are authorized Brokers for Dental, Vision & Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

- Watch our 10 minute VIDEO that explains everything about getting a quote

![]()

By submitting the information below , you are agreeing to be contacted by Steve Shorr a Licensed Sales Agent by email, texting or Zoom to discuss Medicare or other Insurance Plans as relevant to your inquiry. This is a solicitation for Insurance

How to #Estimate MAGI Income for Covered CA?

- From the AGI above, Line 11 Add back in any

- foreign income,

- Social Security benefits and

- interest that are tax-exempt.

- View our main webpage on estimating income

-

- Covered CA Job Aid Countable Sources of Income

- At the end of the year when you file taxes 1040 - you also file Premium Tax Credit Form 8962 to reconcile your estimate with the actual and either get money back or pay more.

- Report changes to income and household status within 30 days, to avoid surprises.

FAQ’s &

Visit our Medi- Cal Webpage

FAQ’s – on FPL Income Chart Frequently Asked Questions”

- Hi Steve,

Been meaning to respond and give you updates. First off, thank you so much for your response back then with great information! You were right on many points.

Thank you again Sara- See our webpage on Introduction to Medicare

- A means test is a determination of whether an individual or family is eligible for government benefits, assistance or welfare, based upon whether the individual or family possesses the means to do with less or none of that help. Means testing is in opposition to universal coverage, which extends benefits to everyone. Means testing increases the administrative burden[1] and can create perverse incentives.[2] Wikipedia

- Federal Changes Toolkits pdf

- Covered CA Toolkits

- Open Enrollment Tool Kit

- Enrollment Dashboard Guide for Certified Enrollers

- FPL Income Chart

- Strike & Lockout

- QLE Major Life Changes

- SEP FAQ's for brokers Covered CA.com

- Documents to Confirm Eligibility

- Income Section

- social press kit.com/lets-talk-health

- Daily Summary Notices Broker Portal

- Medi Cal to Covered CA

- Forms - Including Paper Application

- 1095 toolkit

- how to generate and print plan summaries

- Service & Operating Hours Covered CA.com

- Social Media Toolkit Covered CA.com

- Daily Summary Emails– Notices

- Information Needed

- Understanding Reasonable Opportunity Period (ROP) & Auto Discontinuance Guide

Very informative read…. Your explanation cleared up my confusion.!

https://shuiqi-qishui.cn/

https://www.mchaccess.org/pdfs/training-materials/MCHA%20Income%20Comparison%20Chart%20%202026.pdf

https://www.disabilityrightsca.org/publications/medicaid-policy-changes-in-california-who-what-when-and-why

https://youtu.be/chKtbqR1pC8?si=7hSdVVnlm4uerrIy

https://www.irs.gov/newsroom/avoid-waiting-on-hold-use-irs-online-tools-for-faster-help

Lower income with IRA or HSA

Income thresholds…