Small Employer Health Insurance Business Tax Deduction

for employees, families and owners under

IRC Section §106

Partnerships ** Self Employed ** S Corp ** Schedule 1

Employer Health Coverage Tax #Deduction IRS Section 106

- Group Health Insurance under IRS Code Section §106 is tax deduction as a business expense for both the employer and is not income to the employee. It’s the biggest break there is in the Tax Code, even more so than Mortgage Interest.

- Providing Health Insurance is a GREAT way for EmployER’s to attract and retain better, stable, dependable workers. It’s also the law for large employers (over 50 lives) to meet the mandate and for the employees in CA to meet the individual mandate.

- Internal Revenue Code Section §106

-

Except as otherwise provided in this section, gross income of an employee does not include employer-provided coverage under an accident or health plan.

-

- Internal Revenue Code Section §106

- This allows Employers to deduct Group Health Insurance Premiums for their employees including the owners and officers, as long as it’s a qualifying Group Health Insurance plan as a business expense.

- PLUS, Employees do not have to report employer paid premiums or the benefits in their gross income!

- Scroll down or look to the right of your screen for more references to prove the deduction. Health Coverage Guide *

- If your employees are contributing to the premiums, their portion can also be tax deductible by using a Section §125 POP (Premium Only Plan) or a cafeteria plan.

- Employees whose employers do not currently provide Affordable Group Coverage, might qualify for Tax Credits Subsidies under ACA/HealthReform/Obamacare.

- If the employees on their own want Medical Coverage – like going to Covered CA the premiums are not deductible unless they are more that 10 % of adjusted gross income.

- Writing off medical expenses Publication 502

- Get Employer Health Quotes

- Get Individual & Family Quotes

- See also the Health Care Tax Credit Section 45

- Americans like the employer health benefits tax exclusion: Will it remain under Trump?

The American Benefits Council found most voters back current rules, while America’s Health Insurance Plans found bipartisan support.

IRS #Pub334

Tax Guide for Small Business

Schedule C

-

- IRS Small Business Self-Employed Tax Center VIDEO

- Our FAQ on Meals

-

IRS Small Business Self-Employed Tax Center VIDEO

- How to fill out a Schedule C Profit or Loss from Business VIDEO

- CA Tax Guide for Restaurant Owners

- Taxable and Nontaxable Income Publication 525

- Avalara Tax Compliance Guide for Business 2022 151 pages

- Affordable Care Act Tax Provisions for Employers

- 2024 Tax Reference Guide

Our webpages on

Self Employed

1040 Tax Return – Schedule 1 Line 17

Self Employed Deduction Health Insurance

Self-employed health insurance deduction.

- If you are self employed You may be able to deduct the amount you paid for medical and dental insurance and qualified long-term care insurance for you and your family.

- How to figure the deduction. Generally, you can use the worksheet in the Instructions for Forms 1040 and 1040-SR to figure your deduction. However, if any of the following apply, you must use the worksheet in chapter 6 of Publication #535.

• You have more than one source of income subject to SE tax.

• You file Form 2555 (relating to foreign earned income).

• You are using amounts paid for qualified long-term care insurance to figure the deduction.

- If you got coverage through Covered CA Use Publication #974 Premium Tax Credit instead of the worksheet in the Instructions for Forms 1040 and 1040-SR if the insurance plan established, or considered to be established, under your business was obtained through Covered CA - no extra charge to use an agent and you are claiming the premium tax credit. Publication 334 *

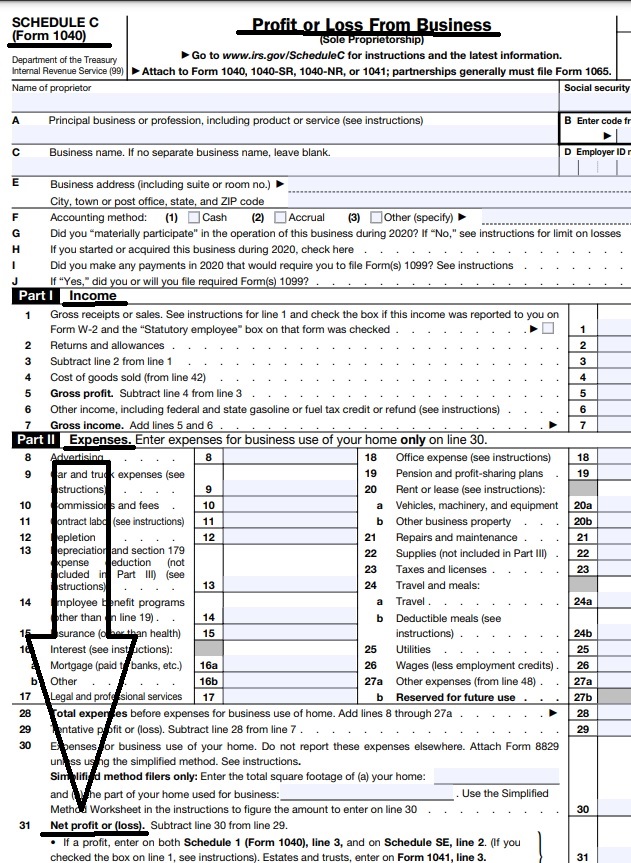

Schedule C 1040 Profit or Loss from Business

Income from your business get's reported for Covered CA MAGI Income subsidies basically by what you put on your Schedule C, line 31 Schedule 1 and 1040 Form .

VIDEO Explanation Part 1 ** Part 2

Line 31 Net Profit or Loss from Schedule C goes on line 3 Schedule 1 of your 1040.

Partnerships

Partnerships

You generally can deduct premiums you pay for the following kinds of insurance related to your trade or business.

- Insurance that covers fire, storm, theft, accident, or similar losses.

- Credit insurance that covers losses from business bad debts.

- Group hospitalization and medical insurance for employees, including long-term care insurance.

- If a partnership pays accident and health insurance premiums for its partners, it generally can deduct them as guaranteed payments to partners. Publication 535 *

The insurance plan must be established under your business.

- For self-employed individuals filing a Schedule C, C-EZ, or F, a policy can be either in the name of the business or in the name of the individual.

- For partners, a policy can be either in the name of the partnership or in the name of the partner. You can either pay the premiums yourself or the partnership can pay them and report the premium amounts on Schedule K-1 (Form 1065)

-

- IRS K 1

- Instructions

- 1065 Partnership Return

- as guaranteed payments to be included in your gross income. However, if the policy is in your name and you pay the premiums yourself, the partnership must reimburse you and report the premium amounts on Schedule K-1 (Form 1065) as guaranteed payments to be included in your gross income. Otherwise, the insurance plan won’t be considered to be established under your business.

- See self employed rules. Ask us for a copy of Q & A # 8747 on Health Insurance for Partners & Sole Proprietors

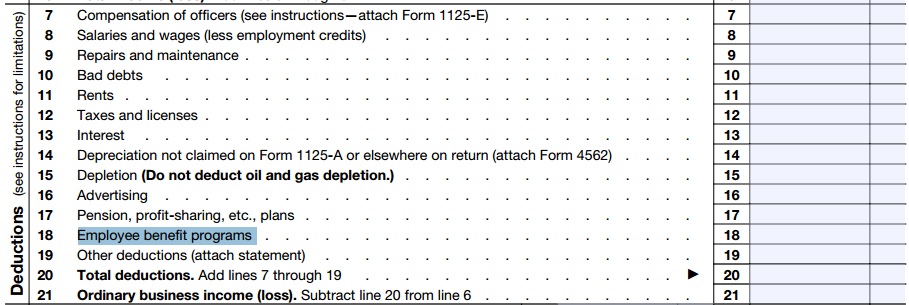

S Corporations

IRS Tax Forms for S. Corp and 2% + plus owners to file for tax deductibility of Group Health Insurance

Section 106 tax deduction for #SCorp Owners?

- The employee premium for S Corporation is not an issue for being tax deductible business expense. See IRS Section 106 above.

- For 2-percent S corporation shareholder-employee it gets complicated and confusing. Check our bibliography belong and competent tax counsel, group health premiums are deductible by the S corporation and reportable as wages on the shareholder– on the employee’s Form W-2, subject to income tax withholding.

- However, these additional wages are not subject to:

- The owner and 2% + shareholders may be able to use the Self-Employed Health Insurance (SEHI) deduction if you’re at least a 2% shareholder in an S Corporation. To claim this deduction, the health insurance premiums must be paid or reimbursed by the S corporation and reported as taxable compensation in box 1 of your W-2. The S Corporation can either purchase the policy in your name or reimburse you for the premiums you paid. The policy can also cover your spouse, dependents, and any nondependent children under the age of 27. See Section 162 IRS Code * (152(f)(1)) * (HR 4872 – Obama Care §162(l)(1)§401(c)(1))

- Claiming the SEHI deduction is generally more advantageous than claiming an itemized deduction. The SEHI deduction will appear on line 17 of Schedule 1 of your federal income tax return, Form 1040 (as part of Line 10), and is limited to the amount in Box 5 (FICA wages by the corporation) of your W-2.W-2 and the K-1 that the S corporation sent to you.

- A 2-percent shareholder-employee is eligible for an above-the-line deduction See Schedule 1 and is able to lower his Adjusted Gross Income (AGI) irs.gov/s-corporation-compensation-and-medical-insurance-issues

- The insurance plan must be established, or considered to be established, under the business. IRS Publication 535 pdf page 18 * If only one employee it can be in employees name IRS.gov * This includes Individual Medicare Plans Journal of Accountancy Check with your CPA.

Links, Bibliography & Resources

-

-

- Source – loop hole lewy.com/health-insurance-deduction

- irs.gov/s-corporation-compensation-and-medical-insurance-issues

- nolo.com/deducting-health-insurance-with-s-corporation

- intuit.com/deduct-health-insurance-premiums-corporation

- S Corporation Compensation and Medical Insurance Issues IRS.gov

- Publication 15B Employer’s Guide to Fringe Benefits..

- IRS Publication 535 Guide to business expense resources

- national underwriter.com/Tax Facts Series

- Question # 8800, 8787, 8804 Email us [email protected] if you would like a copy of those pages.

- 26 U.S. Code § 162 – Trade or business expenses

- (a)In general

There shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business, including—

(1)a reasonable allowance for salaries or other compensation for personal services actually rendered; - Federal Tax Treatment of Health Insurance Expenditures by the Self-Employed: Current Law and Issues for Congress 2009

- (a)In general

- check out Publication #974 Premium Tax Credit,

- If you receive Obamacare Tax Credits, here’s more detail

-

1040 Tax Return – Schedule 1 Line 17

Self Employed Deduction Health Insurance

Self-employed health insurance deduction.

- If you are self employed You may be able to deduct the amount you paid for medical and dental insurance and qualified long-term care insurance for you and your family.

- How to figure the deduction. Generally, you can use the worksheet in the Instructions for Forms 1040 and 1040-SR to figure your deduction. However, if any of the following apply, you must use the worksheet in chapter 6 of Publication #535.

• You have more than one source of income subject to SE tax.

• You file Form 2555 (relating to foreign earned income).

• You are using amounts paid for qualified long-term care insurance to figure the deduction.

- If you got coverage through Covered CA Use Publication #974 Premium Tax Credit instead of the worksheet in the Instructions for Forms 1040 and 1040-SR if the insurance plan established, or considered to be established, under your business was obtained through Covered CA - no extra charge to use an agent and you are claiming the premium tax credit. Publication 334 *

Tax Publications & Guides

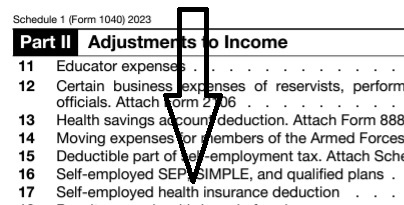

#Adjustments to Income - Schedule 1

#Schedule1 1040

- Part I Additional Income

- 2a Alimony received

- 3 Business income or (loss). Attach Schedule C

- Get Health Quote for your business

- 5 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E

- 7 Unemployment compensation

- 8 Other income:

- a Net operating loss

- b Gambling income

- c Cancellation of debt

- d Foreign earned income exclusion from Form 2555

- e Taxable Health Savings Account distribution

- Part II Adjustments to Income

- 11 Educator expenses

- 13 Health savings account deduction. Attach Form 8889

- 15 Deductible part of self-employment tax. Attach Schedule SE

- Learn more about your Social Security Benefits

- 16 Self-employed SEP, SIMPLE, and qualified plans -

- 17 Self-employed health insurance deduction

- 19a Alimony paid

- 20 IRA Individual Retirement Account deduction

- 21 Student loan interest deduction

- Instant Business Health Insurance Proposals

IRS Publications

- IRS Publication 535 Business Expenses

- IRS Publication 463 Travel #Gift, Meals & Car Expenses

- If I take a client, prospect, my web designer or another member of my profession to pick their brain to lunch, how much is tax deductible?

- GUIDANCE FOR BUSINESS MEALS

allowable business meal expense if:- 1. The expense is an ordinary and necessary expense under § 162(a) paid or incurred during the taxable year in carrying on any trade or business;

- 2. The expense is not lavish or extravagant under the circumstances;

- 3. The taxpayer, or an employee of the taxpayer, is present at the furnishing of the food or beverages;

- 4. The food and beverages are provided to a current or potential business customer, client, consultant, or similar business contact; and

- 5. In the case of food and beverages provided during or at an entertainment activity, the food and beverages are purchased separately from the entertainment, or the cost of the food and beverages is stated separately from the cost of the entertainment on one or more bills, invoices, or receipts. The entertainment disallowance rule may not be circumvented through inflating the amount charged for food and beverages. irs.gov

- GUIDANCE FOR BUSINESS MEALS

- Publication 587 Biz use of Home

IRS Publication 502 pdf * html

Medical & Dental #Expenses

- Aetna Listing of HSA allowable expense

- Corona Virus Costs IRS HDHP

- Can one pay Health Insurance Premiums from an HSA?

- Medical Necessity?

- Insurance Premiums? Deductibility? Publication 502

- Medical expenses include the premiums you pay for insurance that covers the expenses of medical care, and the amounts you pay for transportation to get medical care.

- Medical expenses also include amounts paid for qualified long-term care services and limited amounts paid for any qualified long-term care insurance contract.

- Turbo Tax

- Schedule A 1040 Itemized Deductions

Health Coverage #Guide

Art Gallagher

Health Care Reform FAQ's

Understanding Health Reform

***********************************

Compliance #Assistance Guide from DOL.Gov Health Benefits under Federal Law

- Health Care Reform Explained Kaiser Foundation Cartoon VIDEO

- Choosing a Health Plan for Your Small Business VIDEO DOL.gov

- ACA Quick Reference Guide California Small Group Employers Revision 2020 Word & Brown

- kff.org/health-policy-101/

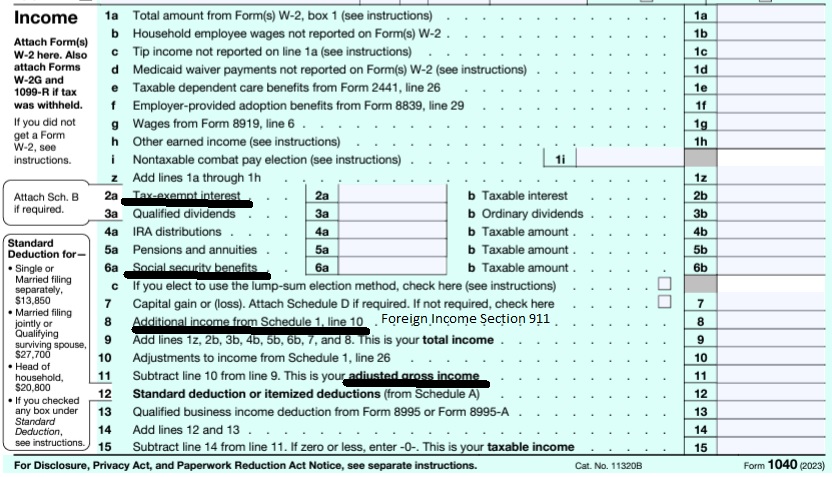

Calculate your Covered CA MAGI Income

take #Line8b 11 Adjusted Gross income then add line 2a, 6a & 8 (Foreign Income)

- 1040 IRS Annual Tax Form

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

- IRA Retirement

- Health Savings Account

- Trumps Big Beautiful Bill - may lower line 6 A Social Security Income Learn More >>> Newsweek * PBS *

- Estimate next years MAGI Income?

- Get instant quotes, subsidy calculation and coverages

- NO ASSET TEST for MAGI based subsidies in Covered CA or MAGI Medi Cal Qualification. Steve's VIDEO

- Nor is there a lien against your estate for Covered CA or MAGI Medi Cal

- Schedule 1 Additional Income & Adjustments to Lower your MAGI Income

References and Technical Links

- IRS More Info on Health Care Arrangements to not have a group plan but pay for employee individual plans. IRS Notice 2013-54

- IRS Publication — Business Expenses #535

- Tax Guide to Fringe Benefits — Publication 15-B

- Internal Revenue Code Title 26 USC

- ⋄Cornell’s Site ⋄

- GPO’s Site

- ⋄Formilab’s Site

- Rev. Rul. 82-196

- Rev. Rul. 67-360

- IRS Withholding Calculator

- CA Franchise Tax Board

- IRS Publication 502(all Medical Expenses) Insurance Premiums

- irs.gov/1040

- Paying into Social Security # 10022

- IRS 8885 Health Coverage Tax Credit A partner with net earnings from self-employment reported on line 15a of Schedule K–1 (Form 1065).

- IRC Section 162 (l)

A shareholder owning more than 2% of the outstanding stock of an S corporation with wages from the corporation reported on Form W–2. - IRS Publication #535 Business Expenses

- Schedule C Profit or Loss from Business 1040

- Instructions Schedule C

- Learn more — No more salary discrimination §2716,

- Tax Estimators

Can you pay an employee NOT to take the group health plan?

Opt out or waiver payment

- You must do a Full Section 125 Cafeteria Plan

- law.cornell.edu/125

- Our webpage on POP Premium only Section 125 Plans

- Reimbursing individual insurance coverage in the ACA era

-

Prior to the ACA, another popular benefit was simply reimbursing employees for individual insurance coverage that they purchased on their own. In most cases, these types of reimbursements could be made on a non-taxable basis. However, as part of the implementation of the ACA, these types of so called “employer payment plans” became largely prohibited, regardless of whether the reimbursements are taxable or non-taxable.

-

-

For the time being, the only ways for an employer to “pay for” individual insurance coverage obtained by an employee is to establish a “Qualified Small Employer Health Reimbursement Arrangement” (QSEHRA) or provide additional taxable compensation, whether though a simple salary increase or a monthly “bonus” or “stipend.” Regarding the additional compensation approach, the key is that the payment not be a “reimbursement”—i.e., not conditioned on proof that the employee indeed obtained his or her own individual insurance coverage. Rather, the increased compensation (regardless of the form) must be unconditional and taxable. Learn More Just Work.com *

FAQ

- 1) I have an employee who has medical coverage through his wife’s employer and her coverage is a group plan not an individual plan.

- 2) The employer requires her to pay for the premium difference between an individual policy and the couples plan they are on.

- 3) When I hired him, he asked if I would cover / reimburse the premium amount that gets taken out of his wife’s paycheck.

- 4) If I elect to pay / reimburse him the amount of premium her employer deducts, is that considered taxable income to him (my employee)?

- 5) Should I add that amount to his salary through payroll or can I write him a separate non-taxable check directly out of my checking account?

.

- 1) That’s great as individual plans can’t be used under ObamaCare by Employer Group’s. HNI

- Since your employee is covered by a spousal group plan, that is a permitted waiver and won’t count as a negative in the minimum participation percentage required by your Insurance Company.

- 2) So, you mean that he’s charging full price for dependents and by individual you mean the employee only rate.

- 3) The wife might check into a Section 125 POP Premium Only Plan or Section 125 Cafeteria Plan (we will be updating that page), so that the portion she pays from her paycheck is tax deductible.

- 4) Here’s a citation Private Letter Ruling 9406002 IRC Section 61 that clearly says you cannot do this, without it being taxable, unless you have a Section 125 Cafeteria plan.

- 5) It would be taxable as salary, unless you have a Section 125 cafeteria plan.

- 3,4 & 5) Does your firm have a group plan that he is eligible for?

- How many employees do you have?

- Are you willing to make this plan available to all employees who can be a dependent on a spousal plan or other MEC Minimum Essential Coverage plan, other than Individual Plans? That is, not discriminate because of salary Section 2716?

- Note that you can’t offer incentives to encourage someone to drop the group plan and take Medicare ADA Cormarkins

- We do not give tax or legal advise.

- Just use and interpret the citations on your own or check with competent professionals.

Brother - Sister - Sibling Side Pages Subpages

View our website with your Desktop or Tablet for the most information

Thank you Steve for all the information. I appreciate it.

We will move forward with deducting it [our health premiums] in taxes.

regards,

Maria

When a corporation pays long term care insurance premiums on behalf of a more than 2% shareholder of an S Corp, and includes that amount as Federal wages on the W-2 Form, should those premium amounts also be reported as State wages on the W-2 Form of an Illinois employee?

Reply

We only practice in CA. Sorry, the links broke for Illinois

See also our pages on Long Term Care benefits not being taxable as income

Tax Qualified Long Term Care Policies

Long Term Care for Employer Groups

See also

aaltci.org/long-term-care-insurance

ltc insurance for owners and executives

Our webpage on w 4 Withholding

Every employer engaged in a trade or business who pays remuneration, including noncash payments of $600 or more for the year (all amounts if any income, social security, or Medicare tax was withheld) for services performed by an employee must file a Form W-2 for each employee (even if the employee is related to the employer) from whom:

Income, social security, or Medicare tax was withheld.

Income tax would have been withheld if the employee had claimed no more than one withholding allowance or had not claimed exemption from withholding on Form W-4, Employee’s Withholding Allowance Certificate. irs.gov/about-form-w-2

WHAT RECORDS DO YOU HAVE TO KEEP TO GET THIS TAX CODE 106 REBATE?

Are you and individual, Sole Proprietor, Self employed, C Corp, S Corp, partnership or what? How many employees are you providing with health insurance?

Here’s instructions for Health Insurance deduction line 24 of your 1120 form on page 13. ===> https://www.irs.gov/pub/irs-pdf/i1120.pdf

Form 1065 for partnerships ===> https://www.irs.gov/uac/form-1065-u-s-return-of-partnership-income

Self employed and S Corp Owners ===>

Can a company offer HIGHLY compensated employees 70% paid health insurance and 50% Aflac insurance and then offer only $450 to the other employees and 0% towards Aflac? I always thought that you had to treat people the same regardless of what the person makes with the exception of Part Time employees. Please help me to clarify this.

Please use the menu above and review the pages on management carve outs, Section 2716 salary discrimination and if you are in CA the get a quote or send your census feature. If you still have questions – please post there.

I elected to put $2400/yr into a dependent care FSA. At the end of June, I had a qualified life event (my husband got a new job and it paid much less than his old job) and my company’s HR dept allowed me to make changes to my benefit elections mid-year. With my husband’s income reduced, we would no longer be able to afford expensive daycare after school, but would need to move to a cheaper option (ASP program at the school instead of private day care), so I stopped contributions to the dependent care FSA. Unfortunately, I already signed the kids up for summer camps in April and May so there was no getting out of that expense. I had $1,200 in my dependent care FSA at the time of this change (1/2 the yr). When I submitted my claims for the summer day camps, they were denied because the camps didn’t take place until July/Aug and I no longer had dependent care FSA coverage. Since I contributed that money, and I’m still with my employer, don’t I have the whole year to use the funds I contributed at the beginning of the year before the qualified life change?

Give us a few days. We will respond on our FSA – Flexible Spending Account Page.

I am employer that funds a HDHP and HSA’s for all employees.

Have employee with an adult child who can no longer be considered a dependent. Adult child needs to open her own HSA but is still covered on HDHP for two more years.

Can employer contribute to adult child’s HSA? If so, are there any tax advantages?

Thank you.

We are creating a new webpage to discuss this issue. Click here to view.