Prescription Drugs – Rx

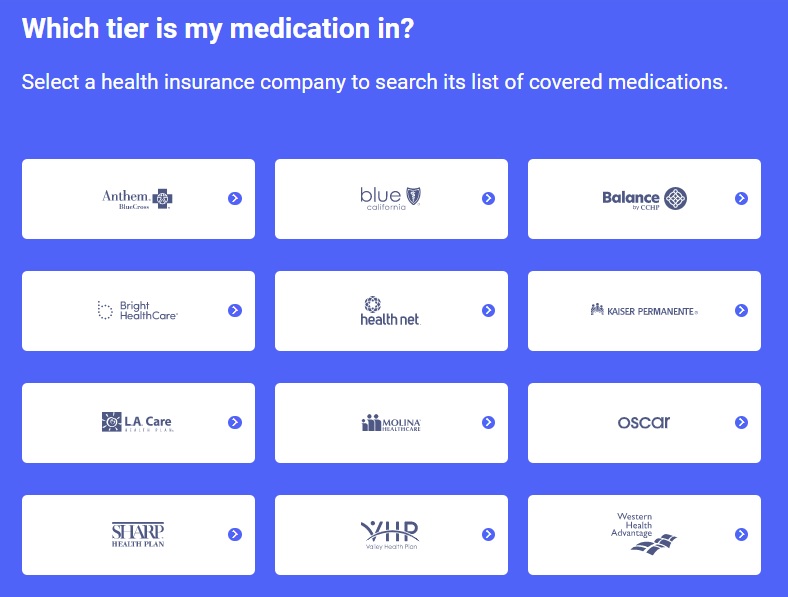

How do I know if my Rx – Prescription is in the formulary – #Covered?

1st What is a Formulary – definition?

The formulary list of preferred Generic and Brand Drugs maintained by the Insurance Companies Pharmacy & Therapeutics Committee. It is designed to assist Physicians in prescribing Drugs that are Medical Necessary and cost-effective. The Formulary is updated periodically. Benefits are available for Formulary Drugs. Non-Formulary Drugs are covered when the Insurance Company or an external reviewer (see our appeals & grievances webpage) approves an exception request. EOC page 110 *

If you are eligible for Medicare Part D Rx, there is a shopping tool that searches all the plans! But, be sure to enroll in the link we give you, so that you get our assistance and consultation in the future.

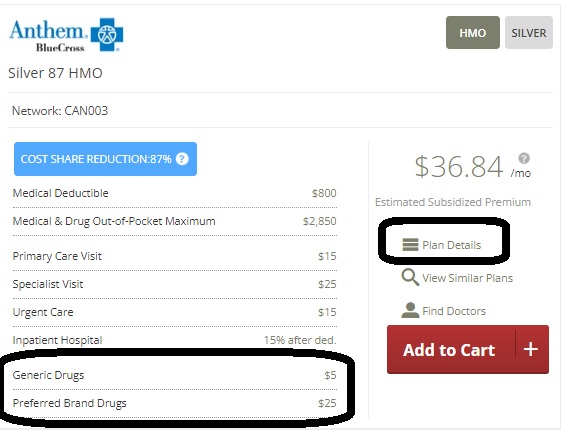

So, go back and check out the FREE quote, click on details, compare up to three plans and see what the co pay is for tier 4

Click on plan details to get more information.

I will grant you that this is a LOT of work.

We can’t stress this enough, the BEST way to find out what YOUR plan covers is in your EOC Evidence of Coverage.

2nd best is our website, 3rd is the one we link to, as it’s a popular plan in CA.

How to request a formulary #exception

- Check the EOC Evidence of Coverage. Here’s Blue Shield’s as an example procedure for Prior Authorization, exceptions & step therapy on page 71 of the EOC

- Oscar Pharmacy Clinical Guidelines (Medical Necessity) We are showing Oscar as IMHO their guidelines are easier to read.

- Some drugs, most Specialty Drugs, and prescriptions for Drugs exceeding specific quantity limits require prior authorization for Medical Necessity, as described in the Prior Authorization/Exception Request Process section. The Member or his/her Physician or Health Care Provider may request prior authorization

- How to get prior authorization is on page 27

- The Member, his/her Physician or Health Care Provider may request prior authorization by submitting supporting information

- For formulary exceptions, the prescriber’s supporting statement must indicate that the non-formulary drug is necessary for treating an enrollee’s condition because all covered drugs on any tier would not be as effective or would have adverse effects, the number of doses under a dose restriction has been or is likely to be less effective, or the alternative(s) listed on the formulary or required to be used in accordance with step therapy has(have) been or is(are) likely to be less effective or have adverse effects. CMS.gov

- Once all required supporting information is received, the Insurance Company will provide prior authorization approval or denial, based upon Medical Necessity, within two business days. Coverage requests for Non-Formulary Drugs in standard or normal circumstances will have a determination provided within two business days or 72 hours, whichever is earlier; the same requests in exigent circumstances will have a determination provided within 24 hours.

- Contacting your insurance company Check their EOC Evidence of Coverage., or the back of your ID card.

- If we are your appointed agent, no charge, we can help you do this, if you send us the supporting documents from your doctor.

- Holistic alternative for erectile dysfunction to Viagra?

Definition of Status of Rx in Formulary List

| Status | Definition |

|---|---|

| Tier 1 | Most generic drugs and low-cost, preferred brand drugs |

| Tier 2 | Non-preferred generic drugs, preferred brand drugs, or drugs recommended by Blue Shield’s Pharmacy and Therapeutics (P&T) Committee based on drug safety, efficacy, and cost |

| Tier 3 | Non-preferred brand drugs, drugs recommended by Blue Shield’s P&T Committee based on safety, efficacy, and cost, or drugs that generally have a preferred and often less costly therapeutic alternative at a lower tier |

| Tier 4 | Drugs that are required by the Food and Drug Administration (FDA) or drug manufacturer to be distributed by specialty pharmacies, drugs that require training or clinical monitoring for self administration, drugs manufactured using biotechnology, or drugs with a plan cost (net of rebates) greater than $600 |

| Non-formulary |

Non-formulary Drugs not listed that meet the Tier 4 description require a formulary exception based on medical necessity to be covered at the Tier 4 share of cost. All other drugs not listed require a formulary exception based on medical necessity for coverage at Tier 3. |

Definition of Restrictions

| Restriction | Definition |

|---|---|

| Age Restriction | Prior authorization may be required if your age does not fall within the FDA, manufacturer, or treatment guideline recommendations. |

| Contraceptive drugs and devices |

Contraceptive drugs and devices covered at no charge. |

| Contraceptive drugs and devices | Contraceptive drugs and devices may be covered at no charge with prior authorization. |

| Gender Limit – Female Only |

Coverage is restricted to females. Prior authorization may be required if the FDA, manufacturer, or treatment guidelines do not recommend the drug for a gender. |

| Gender Limit – Male Only |

Coverage is restricted to males. Prior authorization may be required if the FDA, manufacturer, or treatment guidelines do not recommend the drug for a gender. |

| Limited Access |

Limited Access/Distribution Only available through select pharmacies that are designated by the manufacturer. |

| Limits/Notes | Coverage restrictions or limits for drugs. |

| Prior Authorization | Prior authorization is required to determine coverage |

| Quantity Limit | The prescription quantity covered is limited. Prior authorization is required for greater than the limit. |

| Retail & Mail Pharmacy Access | Tier 4 drugs available at retail and mail order pharmacy. |

| Short Cycle Drug | Short Cycle DrugInitial prescriptions for select Specialty Drugs can be dispensed for a 15 day trial supply. The applicable Copayment or Coinsurance will be pro-rated. |

| Specialty Pharmacy | Must be obtained through a network specialty pharmacy. |

| Step Therapy | Coverage is determined based on use of other first-line therapies/drugs. Copied from BS Website |

Here’s the links to check All the plans in the Individual Market.

How to check the Formulary list.

Let’s not reinvent the wheel, here’s where I did extensive research in April 2022 on how to search Kaiser’s Employer Small Group formulary with VIDEO’s and everything.

Formulary research is one BIG reason not to wait till the last minute to shop plans. If one were to pick a plan at the beginning of Open Enrollment or special enrollment, they have 30 days FREE look, where one could cancel and still have time to pick a NEW plan!

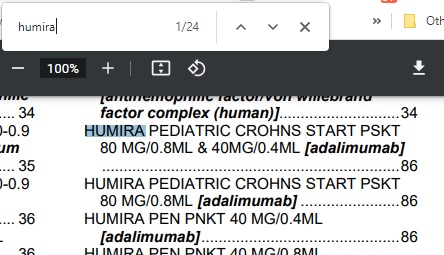

So, just list each Rx in the search box. Then use Ctrl F if appropriate How to use Ctrl F if it’s pdf * VIDEO

How to find what Medications in the Formulary for #psoriasis

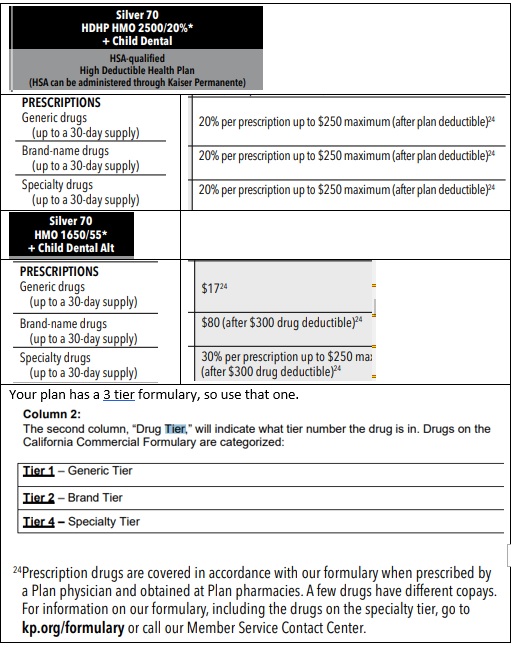

Kaiser Drug Formulary Use the CA Commercial Formulary

I'm checking to verify if your group has a 2 or 3 tier formulary. Also, we will check the Co-Pays and Tiers for your group...

See plan highlights for general information and your co pays

Your group has the option of The Silver 70 HMO 1650/55 and The Silver 70 HDHP 2500/20% HMO

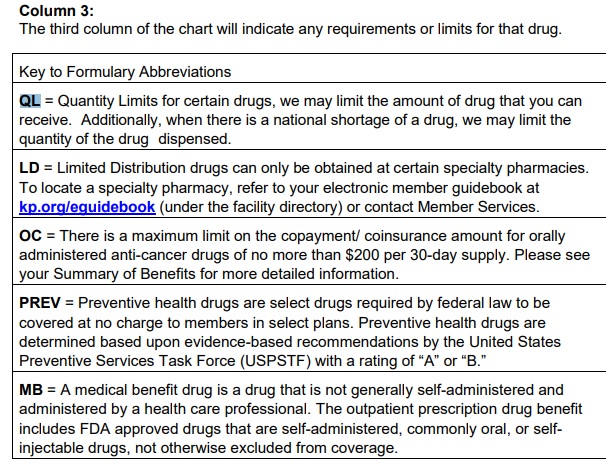

What do the abbreviations mean?

Use Ctrl F to search for the Rx you want to check out

Tier level and quantity level - See highlights above for co pays or just wait till I get the EOC

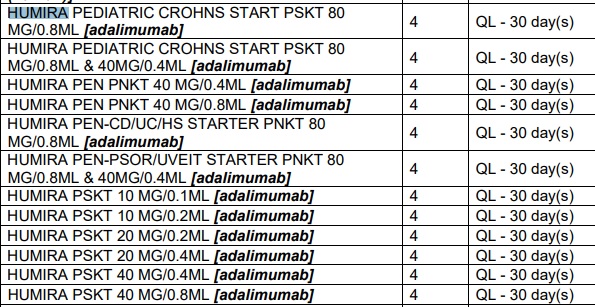

Just as an FYI - See our webpage Q & A for Medicare Part D Rx on Enbrel & Humira

Taltz list price is $6k/month per their website

Kaiser Small Group Evidence of Coverages

Please review the Formulary Exception Process on page 54

EOC #2 - Kaiser Permanente for Small Business Combined Evidence of Coverage and Disclosure Form for {SAMPLE}Kaiser Permanente Silver 70 HMO 1650/55 + Child Dental Alt INFGroup ID: {PID} EOC Number: 2

See also the EOC on grievances - our webpage on grievances and appeals.

I haven't seen where Metal Level has anything to do with the formulary, in fact it's probably prohibited, as only the co pays and deductibles are supposed to be different. Here's where we did extensive research on Flomax and shouldn't it be covered on a Platinum Plan?

FYI - Medicare Part D has a shopping tool, that tells you at ONE time, all the plans and if they cover what prescriptions - I'm not aware of a feature like that for Small Group or Individual.

- Jump to section on:

- Rx Covered?

- Request Formulary Exception

- Pain Management

- Ultra Expensive Rx

- Latuda

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

“Is my prescription on the formulary – approved list?”

- Is #Latuda covered by any Covered CA company?

- What is the co pay?

- See the search instructions

- Getting a formulary exception is beyond our pay grade. Have your doctor review the formulary exceptions above and get the Insurance Company that you want to approve the Rx.

- See also our webpage on continuity of care. While you’re entitled to the same MD, I don’t know about the same Rx and treatment.

- latuda.com/savings Card -and-support Co Pay Card

- What if I’m taking a drug that isn’t on my plan’s drug list when my drug plan coverage begins?

- Generally, your drug plan will give you a one-time, temporary supply of your current drug during your first 90 days in a plan. Plans must give you this temporary supply so that you and your prescriber have time to find another drug on the plan’s formulary (drug list) that will work as well as what you’re taking now, or you or your prescriber can contact the plan to ask for an exception. There may be different rules for people who move into or already live in an institution (like a nursing home or long-term care hospital). Medicare Rx Manual # 11109 Page 30

- Many Health Plans Must Now Cover Full Cost of Expensive HIV Prevention Drugs CA Health Line

Prescription Drug 2025 #RxGuide

PDF # 11109

*****************

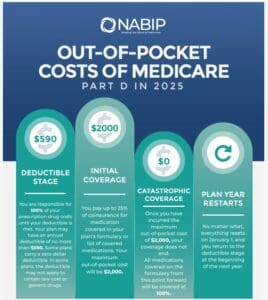

Coverage Gap - Donut Hole $2,000 Cap

******************

- Medicare Part D Rx generally runs say $30 to $100. See link below for how to shop premiums.

- Scope of appointment - permission to discuss Rx and MAPD Plans

- Our Webpage Premiums for those with High Income Parts D Rx & B Doctor Visits

- Medicare Rules for High Income People Medicare Costs # 11579

- Our #High Income Surcharge Video Explanation

- Ways to pay your premium - See brochure above.

- Kaiser Foundation Introduction - Overview

- Fact Sheet Medicare Part D CA Health Care Advocates Hi Cap

-

. Prescription Drugs Hi Cap

- Medicare Part D: An Overview – 10-31-23

- Prescription Drug Resources – 11-07-22

- When Your Part D Prescription is Denied– 11-22-22

- Medicare Rx Benefit Manual Rev 1.2016 83 pages

- Resources: Medicare Drug Coverage (Part D) Mini-Course & Podcast Series CMS

- Network Pharmacies, Formularies & Common Coverage Rules # 11136

- Insulin Maximum Co Pay $35

- Graphic on Part D Premium Increases & Why?

- Maximus Appeals LEP Late Enrollment Penalty

- Shop & Compare Tools Part D Rx

- Get Instant Quotes, Information & Enroll online

- MANDATED wording!: ‘‘We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1–800–MEDICARE to get information on all of your options.’’ § 422.2267(e)(41).

- We disagree with the above wording, as we can use the same tools on Medicare.gov as they do!

Mandated Essential Benefit – ACA/Obamacare

Prescription Drugs – Rx are an essential mandatory benefit of Health Care Reform

Prescription drug benefits.

CFR Code of Federal Regulations §156.122

(a) A health plan does not provide essential health benefits unless it:

(1) Subject to the exception in paragraph (b) of this section, covers at least the greater of:

(i) One drug in every United States Pharmacopeia (USP) category and class; or

(ii) The same number of prescription drugs in each category and class as the EHB-benchmark plan;

California Benchmark Plans

♦ Kaiser HMO 30 (1 Page), ♦ 2 Page, ♦ all plans brochure (30 Pages), ♦ Evidence of Coverage 64 pages

and

(2) Submits its drug list to the Exchange, the State, or OPM.

blueshieldca.com/Standard_Formulary.pdf

(b) A health plan does not fail to provide EHB prescription drug benefits solely because it does not offer drugs approved by the Food and Drug Administration as a service described in §156.280(d) of this subchapter.

(c) A health plan providing essential health benefits must have procedures in place that allow an enrollee to request and gain access to clinically appropriate drugs [medically necessary?] not covered by the health plan.

Please have your MD contact BS to convince them the brand name is the only thing that will work.

800. 535.9481

Fax 888.697.8122

♦ blueshieldca.com/drug-prior-authorization

♦ blueshieldca.com/exceptions-appeals

Procedures shown in “Blue Cross” specimen policy.

Be sure to take your Rx the way your doctor, pharmacist and Rx manufacturer suggest.

Visit Our webpage on Medical Necessity

Holistic alternative for erectile dysfunction to Viagra?

Guaranteed Issue under ACA/Obama Care

All our plans are Guaranteed Issue with No Pre X Clause

Quote & Subsidy #Calculation

There is No charge for our complementary services

Watch our 10 minute VIDEO

that explains everything about getting a quote

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- Get more detail on the Individual & Family Carriers available in CA

Bronze Plan Reimbursement

How are Drugs Rx #reimbursed under the Bronze Plan (Blue Shield)?

The Calendar Year Pharmacy Deductible is the amount a Member must pay each Calendar Year for covered Drugs before Blue Shield begins payment in accordance with the Evidence of Coverage and Health Service Agreement. The Calendar Year Pharmacy Deductible does not apply to all plans. When it does apply, this Deductible accrues to the Calendar Year Out-of Pocket Maximum. There is an individual deductible within the Family Calendar Year Pharmacy Deductible. Information specific to the Member’s plan is provided in the Summary of Benefits.

The Summary of Benefits indicates whether or not the Calendar Year Pharmacy Deductible applies to a particular Drug

If I went to Silver plan,

I pay an extra $120/mo in premium but save $700/mo in prescriptions, rather than

100% up to OOP with bronze plan

- Insure Me Kevin.com Silver vs Bronze

- Pharmacy Cap $500 then 30% ?

- Covered CA on Rx Benefits

- Charge no more than up to $250 per month for one 30-day supply for Silver 70, Gold 80 and Platinum 90 plan members and no more than up to $500 per 30-day supply for Bronze 60 plan members. These costs apply to Tier 4 (specialty drugs). Drugs in lower tiers have lower costs. AB 339 Gordon * CAPG.org * Keenan.com *

- Covered CA Claim Scenarios

- That’s one reason that under Guaranteed Issue ACA – Obamacare you can only enroll at Open Enrollment or if you have a special reason – change of circumstance during the year.

- It’s all a function of the Medical Loss Ratio. Insurance Companies must pay out 80% of all the premiums they take in in claims and can keep 20% for expenses, profit and overhead.

- Holistic alternative for erectile dysfunction to Viagra?

- A service is “medically necessary” or a “medical necessity” when it is reasonable and necessary to protect life, to prevent significant illness or significant disability, or to alleviate severe pain. (2014 ACA Sample EOC Page 166) * Our webpage on Medical Necessity * CA WIC §14059.5

- Get a quote/proposal for your personal situation, including subsidies.

- How does the Blue Shield Matrix (Summary of Benefits – Evidence of Coverage) Explain it?

- Covered CA Explanation from Metal Level Comparison Chart

- The explanation of Rx in the Evidence of Cvoerage is quite extensive, click here to view. We’ve added yellow highlights and bookmarks.

#GoodRx

We do not know who they are. We are not endorsing them. We’ve heard from some of our clients, who are happy with them.

- GoodRx said Wednesday its dispute last year with Kroger continues to affect its bottom line.The company reported a first-quarter net loss of $3.3 million, or 1 cent per share, compared with net income of $12.3 million, or 3 cents per share, a year ago. Quarterly revenue totaled $184 million, down 10%. The company’s biggest revenue driver, its prescription transaction business, saw a 13% decline, to $155.5 million this year from $134.9 million in 2022.GoodRx blamed the decline in the prescription transaction business on its contract dispute last year with Kroger, the national grocery chain that temporarily stopped accepting Good Rx’s discounts at the point of sale in May 2022. The company also blamed the Kroger issue for a 5% decrease in monthly active customers from 6.4 million in 2022 to 6.1 million this year. Modern Health Care *

- Los Angeles Times 9.17.2020 Good Rx going IPO - They can make $$$ since the Rx pricing system is so crazy!

- Times Rx.com

- On the other hand...

“Bronze Plan – How are Drugs Reimbursed?”

Question?

Answer

Question

Pain Management

#Pain Management, Opioid Crisis, Physical Therapy, etc.

- Dr. Oz: How to Treat Chronic Pain Without Drugs

- Breakthrough in the Relief of Chronic Pain Without Drugs!

- Stopping Pain without Rx

- We’re Experiencing a Crisis in Pain Management. Can We Treat It Without Drugs?

- How You Can Manage Your Pain Without Medications With OMT, Acupuncture and an Anti-Inflammatory Diet

Understanding your alternatives - How Can You Relieve Chronic Pain — Without Drugs?

Cognitive behavioral therapy helps guide thoughts, actions - Drug-Free Remedies for Chronic Pain

Escape from pain — without drugs - 8 Proven Ways to Manage Chronic Pain Without Medication

- How to Treat Your Pain Without Drugs

- 8 Surprising (And Natural) Ways To Beat Pain

When it comes to your chronic aches and pains, the new gold standards aren’t what you think - Management of Pain without Medications

- Is it possible to manage pain well without opioids?

- institute for chronicpain.org

- Pain Management Without Drugs

- 11 Tips for Living With Chronic Pain

- practical pain management.com

- Musculoskeletal Health

- Pain Management

- Back Pain

- Arthritis

- The Ache of Arthritis

- Take a tip from the Tin Man

- Anti-Arthritis Diet

- Guide to Posture in the Workplace

- Setting Up Your Workstation

- Repetitive Motion Injury Prevention

- Your Office Workout

- Poster: Keep Motion Injuries at Bay

Mind over Matter

Stress – Seeing a Psychiatrists, Shrink or Therapist

The Ten Biggest Mistakes Psychiatrists Make

6. Don’t refer to therapy.

Psychopharmacology without therapy is treating an infection with Tylenol.

Medications do not cure a psychiatric disease; we’re not even sure what the disease actually is. What they can do is reduce symptoms, give you strength—so that you can learn new behaviors. That’s the point of medications. Treating depression with an antidepressant is not the solution; it’s the preliminary step in allowing you to figure out how to handle depression later on. The adaptation, the adjustment, the physical altering of brain functioning is done by new learning, often this is therapy (though it doesn’t have to be.) I’m not saying therapy is that great, or necessary, either. I’m simply saying that trying to improve a person’s long term status using medications alone without some sort of education and training is a waste of time. It is maybe the most profound disservice of all to tell a patient that their depressive or bipolar symptoms are the result of biology or chemical imbalances and thus absolve them of the responsibility of learning new ways of interpreting and coping with their environment.

8. Polypharmacy

Polypharmacy isn’t just common– it’s the codified standard. When two psychiatrists discuss a patient, inevitably one of them will say these four words: “You should consider adding…” The Last Psychiatrist.com *

- 10 Ways Depression and Anxiety Can Cause Physical Pain

- Can Mental Illness Cause Physical Pain?

- There are indeed mental illnesses that can cause people to experience pain, numbness and a variety of other “physical” symptoms. They are known as Somatoform Disorders.

- Somatic Symptom and Related Disorders Web MD

- New Test Distinguishes Physical From Emotional Pain in Brain for First Time

- 13 Ways That Emotional Pain Is Worse Than Physical Pain

- Is There Such a Thing as Psychological Pain? and Why It Matters National Institute of Health

- The Link Between Depression and Physical Symptoms

- How Emotional Pain Affects Your Body

- Emotional and Physical Pain Activate Similar Brain Regions

Where does emotion hurt in the body? - 5 Ways Emotional Pain Is Worse Than Physical Pain

Why emotional pain causes longer lasting damage to our lives - 8 Physical Symptoms That Prove Depression Is Not Just ‘In Your Head’

We don’t often pair depression with physical pain but research shows this mental illness can really hurt.

Rx – Prescriptions for Pain

- Lumbar Epidural Injections

Therapeutic and Diagnostics Benefits for Low Back Pain - Radiculopathy John Hopkins

- Wikipedia

- Visit our webpage on the clinical guidelines for Rx Medication

Physical Therapy & Exercise

Exercises for the Fifth Lumbar

Rx Drug Abuse

- The Opioid Crisis in America and How Employers Can Help

Medicare Provider Finder https://www.medicare.gov/physiciancompare/

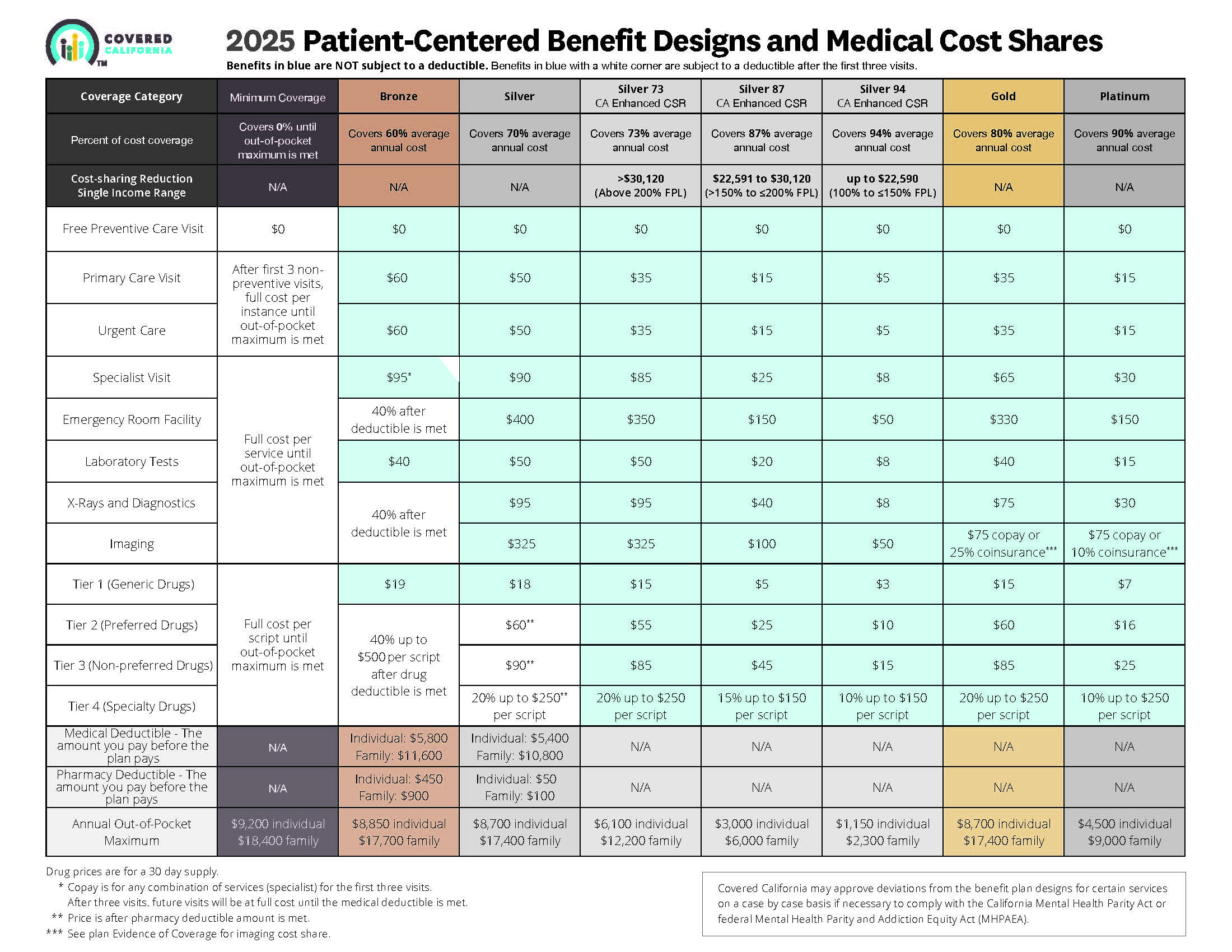

- 2025 Source

- Source and see a sharper image 2024 Patient Centered Designs * *

- Covered CA bulletin on new and improved Enhanced Silver CSR Cost Sharing Reduction

- Do you think your medical bills will be higher or lower than average for your age & zip code?

- Expected Payout (AV)

- MLR Medical Loss Ratio

- Bronze 60%

- Enhanced Silver 70% - 94% Gold 80% Platinum 90%

- Metal Levels are based on Expected Claims Payment - that is the actuarial value (AV).

- Renewal Tool Kit

- Did you notice LOWER deductibles & Co Pays???

- This is one way Health Care Reform hopes to make shopping and comparing Instantly - easier. So, if you get a lower priced plan with less or fewer benefits, co-pays, deductibles you simply pay more when you have a claim. Don't worry, there is a stop loss - maximum out of pocket OOP, of say $7k so that you won't break the bank.

- All plans cover the 10 Federal essential benefits and CA mandated benefits.

- Our main webpage on Metal Levels

FAQ’s

What is the co pay?

Is CVS a participating pharmacy?

You can find your plan summary using this tool plan-summaries.anthem.com/sobdps/

Your PPO plan uses the select drug list.

Here is where Blue Cross shows all their various Rx lists

anthem.com/pharmacy information/

Small Group Select Drug List (Searchable) | (PDF)

WOW, it’s not on the formulary!!!

If my medicine isn’t on the drug list, what are my options?

Here are a few things to think about:

o If you want to take a drug that’s not on the drug list, you may have to pay the full cost for it.

o You can also talk to your doctor or pharmacist to see if there’s another drug covered by your plan that will work just as well, or if generic or OTC drugs are an option. Only you and your doctor can decide what drugs are right for you.

o You can search for generic drugs at anthem.com/ca. OTC drugs aren’t shown on the list.

o If a drug you’re taking isn’t covered, your doctor can ask us to review the coverage. This process is called preapproval or prior authorization. Your doctor can get the process started by calling the Member Services number on the back of your member ID card or by downloading a prior authorization form from our website and submitting it.

covermymeds.com

CoverMyMeds is Anthem’s Preferred Method for Receiving ePA Requests

If your request is approved, the amount you pay for the drug will depend on your plan’s benefit

Insurance Companies are mandated to pay 85% of the premiums in claims. I guess Blue Cross figures if they pay too much for flomax, it will be way over that. 80% Medical Loss Ratio (MLR) – Actuarial Value

APPROVAL CRITERIA for Rx that are not on the Formulary

I. The individual must meet one of the following criteria to receive a non-formulary medication for formulary co-pay;

A. Individual has previously tried and failed 2 (two) formulary products (when available):

One of which has to be in the same specific drug class; the other product can be in a

different drug class however it must have the same indication as the product requested.

OR

B. For combination products: Individual must try two formulary products:

One of which must be in the same specific class as at least one ingredient in non-formulary combination product.

OR

C. For Non-Formulary antibiotics/ anti-virals/ anti-fungals, individual has previously tried and

failed one formulary antibiotic/ anti-viral/ anti-fungal product within the same route of

administration

OR

D. The individual has a documented drug interaction

OR

E. The individual has documented adverse drug experiences (side effects, adverse drug

reaction)

II. Any request for a Non-Formulary prescription medication that does not meet criteria in section I shall be subject to the normal medical necessity review. Source

Alternatives to Flomax???

medical news today.com

Flomax, the branded version of the drug tamsulosin, is often prescribed to relieve the symptoms of BPH. benign prostatic hyperplasia

Flomax can cost more than $200 per month and might not be entirely covered by insurance. Flomax may be no more effective than other alpha-blockers, but the manufacturing company spends more than $100 million marketing it to consumers, so it is often the only BPH drug many people know about.

A generic form of Flomax, called doxazosin, may cost as little as $10 per month.

Resources, Bibliography & Links

- CA Senate Bill SB 853 Wiener 2022 would require state-regulated insurance companies to cover a denied prescription while the patient appeals the decision if a patient has previously taken the drug Read More KHN.org

- New drugs come with high price tag, research finds

- FTC to Investigate CVS Caremark and Other Pharmacy-Benefit Managers

Inquiry will examine what impact their businesses have on cost and access to prescription drugs - Median Launch Price For A New Drug Was $2,115 In 2008. In 2021? $180K

- New drug prices soar to $180,000 a year on 20% annual inflation

- Industry middlemen driving up prices of generic drug prescriptions as much as 20 percent: research

- Legislative leaders to scrutinize state health insurance plan, pharmacy benefit managers

Parent, Child & Related Pages

https://www.cms.gov/medicare/appeals-grievances/prescription-drug/exceptions

https://www.cms.gov/marketplace/about/oversight/other-insurance-protections/prescription-drug-data-collection-rxdc

My pain doctor cut my pain medication down to nothing.

I’m a chronic pain patient what do I do ?

See above for links on Medical Necessity and clinical guidelines

See our links above on pain management and the Opioid Crisis

I have about 8 generic drugs I fill every month. Which is the least expensive plan for drug co-pays?

How do you mean “least expensive?”

The plan with the highest benefits would be Platinum. Platinum would also have the highest premium. It’s all a function of the Medical Loss Ratio, the Insurance Companies, pay out 80% in claims and keep 20% for expenses.

See the Metal Level Chart above. If you qualify for CSR – Enhanced Silver, than 87 or 94 might be better.

When you use our complementary quote engine, you can see all this side by side. See screen shot below.

You might also want to double check each companies formulary, what Rx they pay for at what level.