Small EmployER Group Health & Medical Plans

Get Instant Quotes

Small Group EmployER Health Insurance

Get Quotes

- Employer-sponsored health insurance (ESI) is the largest source of health coverage for non-elderly U.S. residents. Providing health insurance through workplaces is an efficient way of offering coverage options to working families, and the tax benefits of employer-based coverage further enhance its attractiveness. Overall, 60.4% of people under age 65, or about 164.7 million people, had employment-sponsored health insurance in 2023. Kff.org *

- Employer Small Group Plans are now guaranteed issue coverage with just one common law employee (AB 1083), who isn’t a spouse.

- We can also help you with the analysis of employees on a group plan or Covered CA… Learn More>>> Business Insurance.com

- No medical questions are asked!

- Small Business can enroll year around, you do not have to wait for Open Enrollment. See the brochures and other pages in this section of our website, in the menu above and/or the site map, related & child pages.

- Email us [email protected] for more information.

- We are here to help you get the most from your Employer Group Health Plan.

- Our services and consultation are free as long as you appoint us as your agent for no additional charge as we are compensated by the Insurance Companies to help you.

- To learn more about coverage in general, scroll down or see the Health Insurance Guides…

- Get INSTANT Group Proposals

Reasons to get Group Health Insurance

- Recruit better employees.

- Employees stay with you longer.

- Better employee satisfaction

- Save $$$

- Reduce Absenteeism – Employees actually on the job more days, more hours & work more effectively.

- You don’t have to worry about how to pay large medical bills, messing up your credit or filing bankruptcy.

- Piece of Mind

- You know you can get treated when you or a family member is ill or there’s an accident.

- Fixing a broken leg can cost up to $7,500

- The average cost of a 3-day hospital stay is around $30,000

- Comprehensive cancer care can cost hundreds of thousands of dollars

- You know you can get treated when you or a family member is ill or there’s an accident.

- You get the price the Insurance Company negotiates with the doctors and hospitals rather than the list or chargemaster rate.

- Don’t have to be on Medi-Cal.

- Piece of Mind

- The premium that your employer is paying for you, does not show as income on your Tax Return under Section 106

- If you are paying a portion of the premium, that can come off your AGI Adjusted Gross Income so you pay less taxes under Section 125 POP.

- Group Plans may well cost less than an Individual Plan! Don’t forget the tax savings.

- Your employer may be paying 50 – 75 or even 100% of the premium!

- Many options to fit your needs and budget.

- All options cover 10 essential benefits mandated under Health Care Reform.

- There seems to be less chance of losing your coverage with all the political change and court cases.

- Heath Reform Upheld as a tax NFIP vs Sebillius

- Emergency rooms can still send you a bill if you don’t have Insurance and they only have to treat you to resolve the emergency, not total care.

-

- You can have a family doctor and visit him before it’s an emergency. Thus, being preventative and having a healthier and happier life.

-

- Limits on when you can enroll in Individual Health Insurance

- ›

- ›

- Group plans have limits too…

- ›

- People still need insurance. It’s very expensive and difficult to set up a plan

- to pay catastrophic medical bills.

- A lot of people wind up filing bankruptcy when they get in a major accident or severe chronic illness.

- This is what the principle of insurance is all about.

- A lot of people paying a small premium in case of someone having a catastrophic loss. Just like in Little House on the Prairie. If a home burned down, the whole town helped build a new one. See New York Times 11.19.2013 for more information. *

- Piece of mind, don’t have to worry how to pay for a humongous medical bill. Modesto Bee *

- Breakout graphic of $63k Double Bypass & Aortic Valve Replacement Medical Costs have been an issue for a LONG Time Life Magazine 1993

- 2018 Costs health.costhelper.com/heart-surgery *

- 80% Medical Loss Ratio (MLR) – Actuarial Value

- Bibliography

Just Enter your census or securely send us an excel spreadsheet or a list of employees and get instant proposals for California

Bibliography

- How can Covered CA help your Small Business? VIDEO

- why-employees-dont-enroll-in-group-health-coverage

- when- employees reject-health-insurance-plan-at-work

- protection-from-high-medical-costs/

- JPMorgan: How health insurance premiums are impacting small businesses

Resources & Links

- EMPLOYEE BENEFITS AND EMPLOYEE FINANCIAL WELLNESS

- CA Law to comply with Federal ACA AB 1083 2012

- Employer-sponsored health plans can reduce spending on direct medical costs, disability claims, and recruitment and retention, leading to a positive return on investment.

- More Than 1 in 3 Workplace Injury Victims Not Covered by Employer-Based Health Insurance

- 5 reasons why mental health should be a top priority for employers

- Five Truths About How The Inflation Reduction Act Will Help Small Business And Working Families

- Five ways to help your small group clients get the most from health insurance plans

- health insurance is best handled by professionals

- What are the recent trends in employer-based health coverage? KFF 12/2023

- cms.gov/prescription-drug-data-collection

#Insubuy Travel Health Insurance

Instant Quotes, Details and ONLINE Enrollment

Steve talks about International Travel Insurance VIDEO

US State Department - Travel - Insurance

Our webpage on Travel Insurance

https://developers.facebook.com/docs/plugins/page-plugin/

Technical Law & Regulations

Federal ACA/Obamacare

REQUIREMENTS FOR THE GROUP HEALTH INSURANCE MARKET PART 146

Better layout – outline format ecfr.gov

- Subpart A – General Provisions Basis and scope.

- Subpart B – Requirements Relating to Access and Renewability of Coverage, and Limitations on Preexisting

- Condition Exclusion Periods

- 146.111 Preexisting condition exclusions.

- 146.113 Rules relating to creditable coverage.

- 146.115 Certification and disclosure of previous coverage.

- 146.117 Special enrollment periods.

- 146.119 HMO affiliation period as an alternative to a preexisting condition exclusion.

- 146.120 Interaction with the Family and Medical Leave Act. [Reserved]

- 146.121 Prohibiting discrimination against participants and beneficiaries based on a health factor.

- 146.122 Additional requirements prohibiting discrimination based on genetic information.

- 146.123 Special rule allowing integration of Health Reimbursement Arrangements (HRAs) and other account-based group health plans with individual health insurance coverage and Medicare and prohibiting discrimination in HRAs and other account-based group health plans.

- 146.125 Applicability dates.

- Subpart C – Requirements Related to Benefits

- Subpart D – Preemption and Special Rules

- Subpart E – Provisions Applicable to Only Health Insurance Issuers

- Subpart F – Exclusion of Plans and Enforcement

Health Coverage #Guide

Art Gallagher

Health Care Reform FAQ's

Understanding Health Reform

***********************************

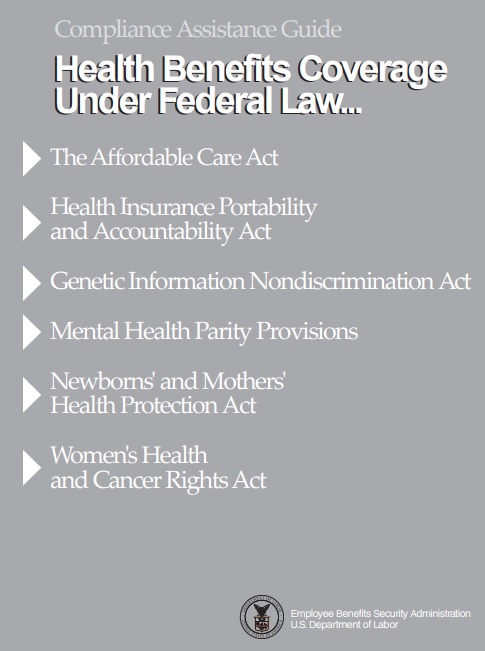

Compliance #Assistance Guide from DOL.Gov Health Benefits under Federal Law

- Health Care Reform Explained Kaiser Foundation Cartoon VIDEO

- Choosing a Health Plan for Your Small Business VIDEO DOL.gov

- ACA Quick Reference Guide California Small Group Employers Revision 2020 Word & Brown

- kff.org/health-policy-101/

Child - Subpages

- Carriers – Companies Employer Group ni

- Aetna Employer Group Plan Coverage

- Blue Cross – Anthem – Employer Health Plans

- Blue Shield – Employer Group

- California Choice – Multiple Companies ONE Bill

- Health Net Employer Small Group

- Kaiser Permanente – New Enrollment – Administrative

- Oscar – CIGNA + Oscar

- Quotes Employer Group – California – Instantly

- Sharp Health Plan

- SHOP – Covered CA for Small Business

- Sutter Employer Health Plans 2022

- United Health Plan UHC Enrollment

- COBRA & California Cal-COBRA 36 months total coverage

- EmployER Definition – Health Care Reform

- Participation & Premium Contribution Requirements

- Tax Credits Small Business §45 R

BROKER ONLY

https://hrdailyadvisor.com/2025/04/07/10-employee-benefits-trends-hr-leaders-should-be-watching/