Disabled Adult Children can stay on Parent’s Health Plan past age 26

California Law – Disabled Child – Health Insurance

CA law allows your incapacitated, handicapped, mentally ill or #disabled child over 26 to remain on the parents group or individual policy, indefinitely, as long as they were disabled before that.

- An individual or group health insurance [“Health Insurance” … shall mean a policy that provides coverage for hospital, medical, or surgical benefits. §106 ] policy that provides that coverage of a dependent child shall terminate when the child reaches age 26 under ACA for dependent children specified in the policy, shall also provide that attainment of the limiting age shall not operate to terminate the coverage of the child while the child is and continues to meet both of the following criteria:

- Incapable of self-sustaining employment by reason of a physically or mentally disabling injury, [AB 88] illness, or condition.

- Chiefly dependent upon the policyholder or subscriber for support and maintenance. Wikipedia Child Support – Maintenance * CA Insurance Code § 10278 * §10277 * for Group Policies Self Insurance Plans §10124 10118

FAQ’s

- Before asking us about this law or if you qualify.

- Please read the law above THREE times and the definition of chiefly dependent below

- Ask your employer’s HR department for the relevant forms and a copy of your evidence of coverage

- For Individual & Family, ask your current broker or Insurance Company to send you the Disabled Dependent Certification and Evidence of Coverage.

- Review the FAQ’s

- What about getting disability income protection for the parents & caretakers?

- Double checking if your child qualifies to stay on your plan?

- What about when employee retires?

- Retirement? Medi Cal – Medicaid?

- COBRA – CAL COBRA when parent retires or quits job?

- I’m changing employers and/or my employer is going with a new Insurance Company

- Same question…

- Self Insured Plans?

- Making changes outside of Open Enrollment?

- Dual Coverage – Medi Cal?

- Would other coverage prevent one from getting dependent coverage under this rule?

- I don’t understand all this and I need private tutoring, education or research, can we arrange that?

- Getting coverage if not on plan prior to age 26?

- How to get documents from the US Department of Labor – ERISA

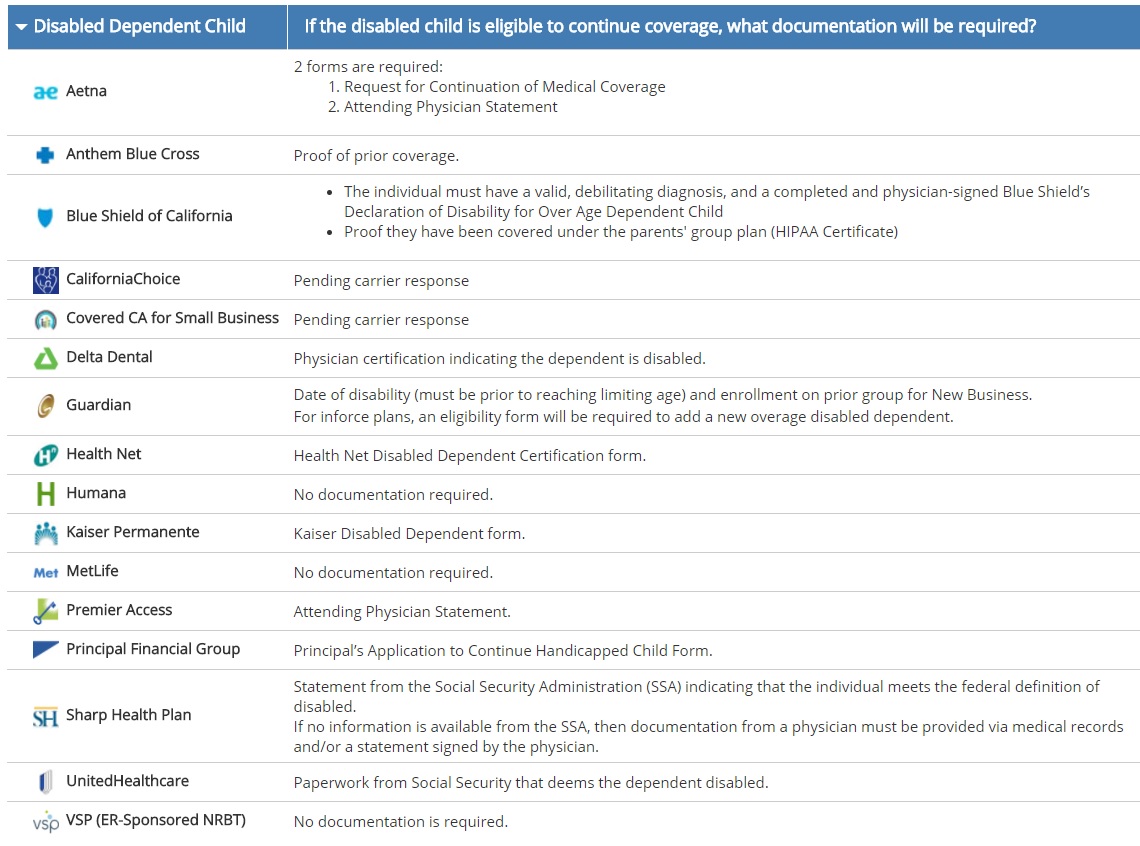

#Proofs Required for Disabled Child – Click to enlarge —

If you have other questions – or want to make sure this is the most current information

Please post in the ask a question area below

- Anthem Blue Cross CA Disabled Dependent Certification

- Sutter Health

- Carriers – Companies Employer Group look for Administrative pages

- Individual & Family Companies – Carriers

FAQ’s

Would an immediate annuity help your situation?

Benefits of Retirement Planning & Effect on MAGI Income

What do the Big Words Above Mean?

What does #ChieflyDependent mean?

“Chiefly dependent” means that the person receives fifty per cent or more of his/her support from his/her parent(s), the insurance contract itself does not define “dependent.” The United States Court of Claims held in Odlin v. U.S., NY.Gov * Covered CA that “chiefly dependent” does not have an explicit definition but rather “each case…must stand upon its own particular facts, and that no hard and fast rule can be laid down arbitrarily fixing the value of property, or the amount of income received…as entirely determinative of the question as to whether [a person] is ‘dependent’ within the meaning of the law.”

While the company’s interpretation of the phrase “chiefly dependent” doesn’t appear to be unreasonable, only a court of competent jurisdiction may make a conclusive determination. Odlin v. U.S. New York State Analysis *

IRS Definition of Dependent section §152. * IRS Interactive Assistant * IRS Publication 501 on Dependents

If your child is dependent on you, consider life insurance to take care of your child when you are gone. Disability in case you get ill and can’t work and Long Term Care, in case you can’t take care of yourself.

In Covered CA, (we are authorized agents) there may be issues with subsidies – MAGI Income.

Considering that everything is guaranteed issue, with no Pre X starting 1.1.2014, I didn’t think this page would be relevant anymore, but it gets a ton of hits!

FAQ’s

- Only disabled say age 25 or after 26?

- Does it matter if it’s Mother or Fathers Employer? Who is child dependent on?

- Marriage?

What is

#Self Sustaining Employment?

- maintaining or able to maintain oneself or itself by independent effort – a self-sustaining community

- maintaining or able to maintain itself once commenced – a self-sustaining nuclear reaction Webster *

- 603. Definition of Substantial Gainful Activity from Social Security Manual

IRC Internal Revenue Code §152(c)(3)(B):

Definition of Dependent

Special rule for disabled.

In the case of an individual who is permanently and totally disabled (as defined in section 22(e)(3)) at any time during such calendar year, the requirements of subparagraph (A) shall be treated as met with respect to such individual.

IRC §22(e):

(3) Permanent and total disability defined.

An individual is permanently and totally disabled if he is unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment which can be expected to result in death or which has lasted or can be expected to last for a continuous period of not less than 12 months. An individual shall not be considered to be permanently and totally disabled unless he furnishes proof of the existence thereof in such form and manner, and at such times, as the Secretary may require. The ABD Team *

- New York State Analysis if Insurer must continue coverage beyond age 26 for disabled child

- IRS Interactive Assistant — who can be claimed as a dependent

- IRS Publication 501 – Tax Filing Status – Search for rules on determining support

FAQ’s

Sample Policy & How to Read & Interpret It

Specimen Individual Policy #EOC with Definitions

Employer Group Sample Policy

It's often so much easier and simpler to just read your Evidence of Coverage EOC-policy, then look all over for the codes, laws, regulations etc! Plus, EOC's are mandated to be written in PLAIN ENGLISH!

- Find your own Individual EOC Evidence of Coverage

- It' important to use YOUR EOC not just stuff in general!

- Obligation to READ your EOC

- Plain Meaning Rule - Plain Writing Act

- Our Webpage on Evidence of Coverage

- OOP Out of Pocket Maximum - Many definitions are explained there.

VIDEO Steve Explains how to read EOC

Excerpt from “typical” Group plan:

4) If coverage for a Dependent child would be terminated because of the attainment of age 26, and the Dependent child is disabled and incapable of self-sustaining employment, Benefits for such Dependent child will be continued upon the following conditions:

a) the child must be chiefly dependent upon the Subscriber, spouse, or Domestic Partner for support and maintenance;

b) the Subscriber, spouse, or Domestic Partner must submit to Blue Shield a Physician’s written certification of disability within 60 days from the date of the Employer’s or Blue Shield’s request; and

c) thereafter, certification of continuing disability and dependency from a Physician must be submitted to Blue Shield on the following schedule:

i. within 24 months after the month when the Dependent child’s coverage would otherwise have been terminated; and

ii. annually thereafter on the same month when certification was made in accordance with item (1) above. In no event will coverage be continued beyond the date when the Dependent child becomes ineligible for coverage for any reason other than attained age. * [See also Conditions of Enrollment Page B 56 * Dependent Definition Page B 70] EOC

Guide to #Contract Interpretation

#Plain Meaning Rule

How to read a policy

How to read and figure out the law or Insurance Policy Provisions - Evidence of Coverage

- Read the Statute – Policy

- Read the Statute – Policy

- Read the Statute – Policy

- Then when you think you understand it, read it again

-

-

- Then as my cousin reminded me - one needs to check Westlaw, Google or the Talmud to see how the courts have interpreted the law, their might be some jiggery pokery - malarky going on.

- Check your Insurance Company Evidence of Coverage EOC one big advantage of the EOC is that it's in Plain English.

- Scroll down for more...

- Felix Frankfurther – Wikipedia

-

-

- Then when you think you understand it, read it again

- Tools to Read a Statute VIDEO

- Contract Interpretation in California: Plain Meaning, Parol Evidence and Use of the Just Result Principle

-

More on How to read a contract - Insurance Policy

-

The language of the text of the statute or Evidence of Coverage EOC should serve as the starting point for any inquiry into its meaning. To properly understand and interpret a statute, [first] you must read the text closely, keeping in mind that your initial understanding of the text may not be the only plausible interpretation of the statute or even the correct one, per Justice Felix Frankfurter . Guide to Reading & Interpreting * American Society of Healthcare Risk Management and * Wikipedia.

-

The starting point in statutory construction is the language of the statute - Evidence of Coverage itself. The Supreme Court often recites the “plain meaning rule,” as in, King vs Burwell Subsidies in Health Care.Gov upheld, that, if the language of the statute is clear, there is no need to look outside the statute to its legislative history in order to ascertain the statute’s meaning.

-

Parol Evidence Rule Wikipedia - Contract stands by itself - can't bring up discussions or agreements that were prior to actually signing the written Contract

-

The plain meaning of the contract will be followed where the words used—whether written or oral—have a clear and unambiguous meaning. Words are given their ordinary meaning; technical terms are given their technical meaning; and local, cultural, or Trade Usage of terms are recognized as applicable. The circumstances surrounding the formation of the contract are also admissible to aid in the interpretation. West’s Encyclopedia of American Law,

-

A cardinal rule of construction is that a statute should be read as a

Harmonious Whole,

with its various parts being interpreted within their broader statutory context in a manner that furthers statutory purposes. A provision that may seem ambiguous in isolation is often clarified by the remainder of the statutory scheme — because the same terminology is used elsewhere in a context that makes its meaning clear, or because only one of the permissible meanings produces a substantive effect that is compatible with the rest of the law.”

-

In Edgar v. MITE Corp., 457 U.S. 624 (1982), the Supreme Court ruled: “A state statute is void to the extent that it actually conflicts with a valid Federal statute.” In effect, this means that a State law will be found to violate the supremacy clause when either of the following two conditions (or both) exist:[3]

- Compliance with both the Federal and State laws is impossible, or

- “…state law stands as an obstacle to the accomplishment and execution of the full purposes and objectives of Congress…”

Supreme Court - FINAL Ruling - Plain Meaning - No Jiggery Pokery 47 Pages, view our highlights, annotations & bookmarks

Our webpage on

- jiggery pokery and contract interpretation

- Evidence of Coverage EOC

- Plain Meaning Rule - How to read Policy - Contract

Social Security Disability – For Comparison Purposes – Can’t Work?

#SocialSecurityDisability

Factors in Evaluating

Parents & Care Givers

Check out our webpage on getting your own private disability coverage, in addition to Social Security Disability or SDI State Disability Coverage

- Disability Income – Pay Check Protection

- SSI – Supplemental Security Benefits – Automatic Medi Cal – SSDI

FAQ's

- Deafness?

- Mental Health – ACA/Health Reform Mandated Essential Benefit

- nolo.com/guide-to-social-security-disability

- c:/medi-gap/Social Security/disability

All our plans are Guaranteed Issue with No Pre X Clause

Quote & Subsidy #Calculation

There is No charge for our complementary services

- Kaiser Foundation estimator for 2026... Use till 10/1/2025 when we get the new rates and subsidies loaded into our Quotit Calculator

- We are authorized Brokers for Covered CA get instant quotes direct and in Covered CA with subsidy calculation for:

Watch our 10 minute VIDEO

that explains everything about getting a quote

-

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

Employee’s guide to #COBRA –

Department of Labor

- EmployER's Guide to COBRA

- DOL on Health & Retirement benefits after job loss

- DOL on COBRA

- Legislation to make COBRA credible coverage

- FAQ CA Department of Insurance

- CA Department of Managed Health Care FAQ's

- Retirement and Health Care Coverage... Questions and Answers for Dislocated Workers

- Federal workers hit by layoffs have their own version of COBRA

Here's what private-sector benefits specialists should know about new hires coming in with "temporary continuation of coverage" benefits. - Navigating COBRA Continuation Coverage: What Employers and Brokers Need to Know

- Your Employer's Bankruptcy – How Will It Affect Your Employee Benefits?

*********

Art Gallagher Employers Guide to COBRA

- Our Webpage on COBRA & Cal COBRA

- Get Individual Guaranteed Issue ACA/Obamacare Quotes -

- Subsidies if you make less than 600% of Federal Poverty Level!

- No Pre X Clause!

- No wait for Open Enrollment as you get Special Enrollment when you lose COBRA or your Employer Group Plan!

- #Social Security Disability Benefits Publication # 10029

- SSI Introduction Publication # 5-11000

- More than you ever wanted to know on SSI

Understanding SSI Publication # 17-008 120 pages - SSI in CA #11125

- What every woman should know Publication 10127

- 1 hour lecture

- Our webpage on

#Attorney 's that can help you through the Social Security Disability maze

- west coast disability.com/

- CA State Bar Attorney Referral Service

- Legal Match.com

- Sellers Law

- Hill & Ponton

- premier disability.com

- Cantrell & Green

- We don't necessarily know these attorney's...

- Editorial: Lawyers are fighting innovative proposals for more affordable legal assistance. That’s wrong LA Times 1.30.2022

- We don't necessarily know these attorney's...

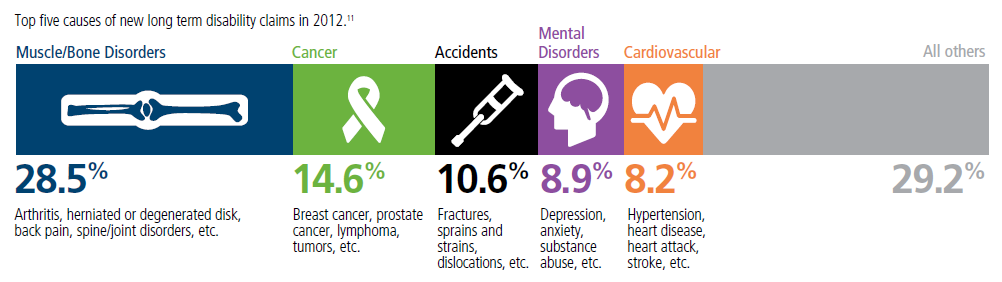

Top 5 - 10 causes of Long Term Disability Claims

Lower back disorders ♦ Depression ♦ Coronary heart disease, arthritis and pulmonary diseases (Met Life) ♦ Disability Can Happen ♦ CDC Statistics

Our webpage on Disability Payments - Insurance

Get Disability Quotes for Parents, Caretakers & Wage Earners

What Parents Need to Know about #Special Needs Trusts

VIDEO

Trans America

Special Needs Trust Brochure

#Nolo Special Needs Trusts

- Get Life Insurance Quote to fund the trust

- Our webpage on Special Needs Trusts

- Social Security Publication 10076 Guide for Representative Payees

- FAQ's

- When does the trust actually get funded, go into place, become effective?

- See page 47 of Nolo's book on Special Needs Trusts - The best known way is to specify what assets go into the trust at your demise. Be careful of probate, page 48. See Revocable Living Trusts on Page 50. Where a living trust can fund a Special Needs trust at your passing. See page 140 about actually creating the Special Needs Trust

- See chapter 2 for what payments and benefits the child can get

- See page 47 of Nolo's book on Special Needs Trusts - The best known way is to specify what assets go into the trust at your demise. Be careful of probate, page 48. See Revocable Living Trusts on Page 50. Where a living trust can fund a Special Needs trust at your passing. See page 140 about actually creating the Special Needs Trust

FAQ’s

What about #Selfb Insured Plans?

Answer: What does the evidence of coverage – EOC say?

Please send your EOC to us or at least take a photo of your ID card with your Smart Phone and send to us. We don’t post individual identifiable information. We might then be able to search and find your EOC Evidence of Coverage and it would be so much easier to show you the benefits you have in your policy.

Pro

The Affordable Care Act, also known as the ACA, specifies requirements and guidelines in a number of different areas that are relevant and applicable to self-funded employers. Below is a summary of these provisions.

Disabled children who meet the requirements for enrollment, however, do not become ineligible at age 26. Providence.org

ADA NCBI.NLM.NIH.gov

The ADA protects against disability-based discrimination in employment, governmental and commercial activities, transportation, and telecommunications.

ADA Title V allows bona fide insured or self insured employee benefit plans to make some health-related distinctions for risk classifications based upon, or not inconsistent with, state law.

However, all such provisions are allowable under the ADA only if they meet the requirements of applicable state law and are not used as a subterfuge

Disability-based distinctions involving dependent coverage will be analyzed in the same fashion as disability-based distinctions in employee coverage Cornell.edu

The Department of Labor has instituted disability nondiscrimination regulations which may apply to those with “health factors.” The regulations are complex; setpnowskilaw.com

Con

CA Department of Insurance does not regulate Self Insured Plans Insurance.CA.Gov

Self-funded Health Plans–Federal or Governmental:

Although the business of insurance is primarily regulated by the state, a number of federal laws contain requirements that apply to private health coverage, including ERISA and HIPAA. ERISA was enacted in 1974 to protect workers from the loss of benefits provided through the workplace; and in 1996, HIPAA was motivated by concern that people faced lapses in coverage when they change or lose their jobs.

Most self-funded health plans operate under ERISA and are health benefit arrangements sponsored by empoyers or employee organizations. Under a self-funded arrangement, the employer retains the responsibility to pay directly for health care services of the plan participants.

In Connecticut, self-funded health plans cover approximately 50% of the privately insured citizens.

ERISA does not require employers to establish any type of employee benefit plan, but contains requirements applicable to the administration of the plan, such as requirements for disclosure, reporting and fiduciary standards, claims and continuation coverage.

In general, ERI[S]A preempts state laws that would regulate the operation of health plans. Therefore, any state mandates do not apply to those covered by self-funded plans. (An exception is CT’s state employee plan, which abides by state mandates by contract).

Self-funded governmental plans such as the state employee plan or municipal self-funded plans may be exempt from ERISA but still bound to follow other federal laws, such as the federal regulations on internal and external review processes under the Affordable Care Act or the Mental Health parity and Addiction Equity Act of 2008. Ct.Gov

Can my child with a disability be covered after the age of 26?

If your plan is fully insured, it is regulated by state laws in addition to federal laws Pacer.org

ERISA

What about Governmental or Church plans, does ERISA affect those?

See our Page on ERISA

See 29 US Code Section 1003 (b)

The provisions of this subchapter shall not apply to any employee benefit plan if—

(1)such plan is a governmental plan (as defined in section 1002(32) of this title);

(2)such plan is a church plan (as defined in section 1002(33) of this title) with respect to which no election has been made under section 410(d) of title 26;

***************

Excerpt of Blue Cross Small Business Application

************

Cal PERS We serve those who serve California. California Public Employees’ Retirement System

Forms, Information and Rules on Disabled Children over 26

Questionnaire

Doctors Medical Report

*****************

Links & Resources

- Mental Health Benefits are an essential benefit under Health Care Reform.

- Dental Coverage can be purchased here.

- Dual Coverage – Which Insurance Company pays first? Medi-Cal, SSI, SSDI? Medicare, Private, Employer?

- Special Needs Trusts

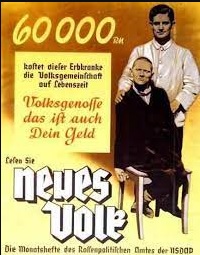

Hitler & Mental Health Disabilities T 4

Speak up! Do want you can to make sure this doesn't happen in the USA!

Translation for the poster below:

"This person suffering from hereditary defect costs the community $60,000 Reichsmark during his lifetime. Fellow German, that is your money, too. Translation & Image Courtesy of Psychology Fantom.com

Under the T 4 program, wikipedia.org T4 Certain German physicians were authorized to select patients "deemed incurably sick, after most critical medical examination" and then administer to them a "mercy death" (Gnadentod).[7] The T4 programme stemmed from the Nazi Party policy of "racial hygiene", a belief that the German people needed to be cleansed of racial enemies, which included anyone confined to a mental health facility and people with simple physical disabilities.[31] wikipedia.org T4

The annual cost for a bed in a CDCR-operated, inpatient psychiatric program is around $301,000 lao.ca.gov *

Did President Trump??? really say and mean this? Time.com

FAQ’s

- Question Hi! I’m 26 years old, and on my mom’s insurance as a disabled dependent due to my medical condition. Medical documentation confirmed all approved months ago.

- However, I just applied for a part-time position at her work hoping to at least contribute some hours.

- Would working part time jeopardize my disability approval on her insurance?

- Is it safe to just not work at all?

- My health insurance is the most important thing I have due to my medical disability, # of doctors, and treatment.

- But I’d also like to contribute somewhat financially if I can.

- The job would be part-time so it’s ineligible for benefits. But I wouldn’t take it if it could mean jeopardizing my health coverage. I can’t risk not affording my medical care.

- However, I just applied for a part-time position at her work hoping to at least contribute some hours.

- Response

- The issue isn’t if you have a part time job, but if you are capable of Self Sustaining Employment?

- 603.1 What Does Substantial Gainful Activity Mean?

- The term “substantial gainful activity” is used to describe a level of work activity and earnings.

-

Work is “substantial” if it involves doing significant physical or mental activities, or a combination of both.

-

“Gainful” work activity is either of the following:

-

Work performed for pay or profit;

-

Work of a nature generally performed for pay or profit; or

-

Work intended for profit, whether or not a profit is realized.

-

-

603.2 Does Work Need To Be Performed On A Full-Time Basis To Be Considered Substantial Gainful Activity?

- No. For work activity to be substantial, it does not need to be performed on a full-time basis. Work activity performed on a part-time basis may also be substantial gainful activity. (See §§618-621.) ssa.gov *

- 603.1 What Does Substantial Gainful Activity Mean?

- So, maybe 6 months ago you were disabled, but maybe not now. I can’t say. If you are able to work and lose your group coverage, you can get ACA/Obamacare if you make more than say 20k or Medi Cal if you make less. Get Quotes!

- Why stay home and do nothing, if you can be independent?

- Insurance companies often require annual certification of disability.

- The issue isn’t if you have a part time job, but if you are capable of Self Sustaining Employment?

https://youtu.be/gpQQuGHD73Q?si=W5O6N-91jfrRLBaN

My disabled child is aging out of my group health insurance policy. She received COBRA notification with an expensive monthly premium, more than my usual monthly premium. Would keeping her on as a disabled adult dependent subject her to the COBRA premium?

If you can provide the proofs for your child to stay on the plan, the premium would be the same as before.

Can you tell me if having private insurance to continue after my adult child turns 26 vs medi CAL is a good idea?

My young adult will be considered disable dependent

***Are you sure?

under my private insurance.

Is there any disadvantage of having her “locked” into private insurance for the life of my husband and I?

***Who says she’s locked in? You should be able to change at open enrollment.

https://www.shrm.org/topics-tools/tools/hr-answers/annual-open-enrollment-period-employee-health-insurance-benefits-required

I’m not aware that Medicare will add your daughter, unless she qualifies on her own. Namely SSDI after two years.

If the link requires password, let me know.

I don’t see any problem with your daughter having Medi Cal and Employer Group Coverage. Employer Group pays first. See our webpage on that.

Hi

I have a 29 yr old daughter who has been disabled since the age of 7. My insurance through work dropped her off my plan once she turned 26. I was unaware of kids w/ disabilities being able to stay on insurance plans and when I called my job to inquire they said I had to have signed forms before her turning 26 and have the board review and determine if she could stay on my insurance. Is there anyway to overturn or refute this? Thank you!

See Insurance! code 10277 section B they have to notify you.

(b) The insurer shall notify the employee or member that the dependent child’s coverage will terminate upon attainment of the limiting age unless the employee or member submits proof of the criteria described in paragraphs

(1) and

(2) of subdivision (a)

to the insurer within 60 days of the date of receipt of the notification.

The insurer shall send this notification to the employee or member at least 90 days prior to the date the child attains the limiting age.

Upon receipt of a request by the employee or member for continued coverage of the child and proof of the criteria described in paragraphs (1) and (2) of subdivision (a), the insurer shall determine whether the dependent child meets that criteria before the child attains the limiting age. If the insurer fails to make the determination by that date, it shall continue coverage of the child pending its determination.

How are you gonna prove they didn’t? I don’t know because they’ll probably say they did. Check our webpage on USPS Informed Delivery.

I have a Dependent Adult Child w a Mental disorder, who requires her Psychiatrist MD to sign an HBD-34-Calpers 2926 insurance extension form 4 pages lo g.

Who refuses because “.. I’ve never had to do one before!” and won’t start anytime soon.

The problem is my daughter only has one week left before the deadline. This will force her both psychologically and financially into the streets of LA.

insurance company says hands are tied and my daughter needs a Medical provider to sign off on it to have her remaining on our health insurance.

What recourse or options do we have? Legally? Appeal?

The quick and simple answer is get Medi Cal & SSI

Where is your daughter living now?

Are you supporting her?

Check these websites…

Get me a full copy of the evidence of coverage for your policy.

How about if your MD just attaches the medical records, but doesn’t fill out the form? It’s your right to have access!

Our webpage on finding a therapist

How about getting an Individual Obama Plan?

Watch this page for more…

If a disabled adult child (DAC) woman receiving SSDI through the pickle program

marries a man with no income because of his own disability and is not on SSI or SSDI

because he has affluent parents that make enough to care for him,

will the DAC women lose her monthly SSDI income and medical that her and her toddler relies on?

Thank you so much

This seems to be a rather complex question. We just got back from vacation and now caught a cold. It might be awhile till we can truly research this. We are not compensated to have this website…

In the meantime, see our pages on:

Pickle Program

SSDI

Medi Cal contact

DAC Disabled Adult Child Program

CA Health Care Advocates – SHIP HI-Cap

It appears the the pickle amendment only protects you to keep Medi Cal. Your daughter is probably qualified under MAGI Medi Cal, meaning that your income is below 138% of federal poverty level.

How much is your fiancé’s father “gifting” him per year?

Is he paying gift tax?

Is he claiming him as a dependent?

Here’s our webpage on gifts as income?

Your question is really above our pay grade. Try calling the people on the Medi Cal contact page listed above

Maybe this company can help you? https://www.medi-caladvisorgroup.com/ or this one

https://www.medihelper.com/

Thank you for making time.

My son is 32 and disabled and on my Aetna plan as a disabled adult. I will be turning 65 soon and thus going on Medicare. Will he loose his coverage under Aetna? If I choose a supplemental Aetna medicare plan, will he be able to stay on Aetna?

Is your Aetna Plan an Individual or a Group Plan?

If a Group Plan, will you still be working?

No, a Medicare Plan won’t cover your son.

We live in CA, our son is 28 and therefore came off our insurance two years ago.

He is autistic and we didn’t realize he might still be eligible to remain on our policy (through my employer – bcbs ppo) indefinitely as we support him as he is unemployed/underemployed due to autism.

Are autistic children eligible and if so how absolus we proceed?

Please contact your employer’s HR department and get a copy of the evidence of coverage and the forms, then we can review and see.

It doesn’t seem that the question has been asked before about their being a lapse in coverage.

It’s not if autism is covered, it’s if your son is chiefly dependent on you and is incapable of self sustaining employment.

https://disability.lacity.org/

kff.org medicares-role-for-people-under-age-65-with-disabilities/

https://www.anthem.com/ms/easyrenew/Handicapped_Dependent.pdf

May i enroll my adult son with a disability on my current health insurance plan?

We need a copy of your EOC Evidence of Coverage to get you a true, correct & verified answer.

How old is your son?

When did he first become disabled?

Is he on your plan now?

Does he meet the two requirements under the law above to qualify?

What Insurance Company and Plan are you with?

Can you complete their forms?

What about Medi Cal?

ACA/Obamacare Guaranteed Issue?

I have a disabled son aged 32 years, who is covered under my employer’s group health insurance plan as the primary and Medicaid as the secondary insurance.

He has been disabled since birth and has been on my employer’s group health insurance plan prior to age 26. He requires to undergo a medical procedure that is not covered under my employer’s plan but covered under Medicaid.

I would like to temporarily terminate my son’s coverage from my employer’s health plan and continue with Medicaid so that he can have his procedure done.

Can I do that?

If so, can I re-enroll my son in my employer’s plan after the procedure?

Do NOT cancel the Employer Plan!

While your Employer Plan is primary, that just means they get billed first. So, if the Employer Plan pays nothing, then Medi Cal will get the bill. It does NOT mean, that you have to go to MD’s on the Employer Plan first!

I’m sure if you ask Rando’s at the Insurance Company or Medi Cal, they will tell you something else, but unless they can show it to you in writing, IMHO it’s not worth the dime to call them.

See our webpage on Dual Coverage.

You may not quote anything I say or that you think I say. You may only refer to the actual footnotes to the law or actual Insurance Company EOC Evidence of Coverage.

I don’t have a choice. I lost my job. How – Can I get my child on an employer plan when I do get another job, being as the new employer didn’t have her covered before age 26?

I would have to read the law another 3 times along with the law on COBRA & Cal COBRA. Plus, review the EOC from the old and new employer. Maybe keeping your child on COBRA would make it continuous coverage, before age 26?

If the employee or member changes carriers to another insurer or to a health care service plan, the new insurer or plan shall continue to provide coverage for the dependent child. CA Insurance Code 10277 (d)

(d) If the employee or member changes carriers to another insurer or to a health care service plan, the new insurer or plan shall continue to provide coverage for the dependent child. The new plan or insurer may request information about the dependent child initially and not more frequently than annually thereafter to determine if the child continues to satisfy the criteria in paragraphs (1) and (2) of subdivision (a). The employee or member shall submit the information requested by the new plan or insurer within 60 days of receiving the request.

I am widowed and employed by a city, who has continued to keep my special needs daughter on after the age of 26.

I am retiring in about 2 years and I receive retirement health care.

How long does my daughter get to stay on? when I retire? or social security age? or death?

Please help?

Assuming that you are in CA, the law says that your daughter can stay on as long as you are covered by the policy.

Please see our page on interpreting law, rules & statutes. Also, see our page on the importance of reading the actual policy, EOC Evidence of Coverage.

I would really need to see all your retirement materials to verify that your daughter would be covered under that plan. I don’t see that your Social Security age would be relevant. If you G-d forbid die, then your daughter would lose coverage under your plan. She could take COBRA and Cal COBRA for 36 months. She would qualify for a guaranteed issue, no pre x individual plan…Get Quotes. If no income, then Medi Cal or she could pay the full price of an individual plan without subsidies.

Check out life insurance to help take care of her, should you pass.

Hi, I have a 24 yr old with schizophrenia, and run across your web site trying to find resources for them (specifically a Special Needs Trust which I just had learned about).

I wanted to ask questions about signing them up for Medi-Cal and accessing LA County resources for mental health.

My kid is covered by Blue Cross PPO through my policy which is with USC.

I would love to discuss also how to prepare to get my kid coverage after my policy does not cover them once they are 25 years old, or maybe my kid needs to file for disability in order for my policy to cover what they need.

Would love your help with all these topics! I never knew that people like you existed…

Thanks for all the resources on your web site, and look forward to hearing from you.

I don’t see any reason why USC would not continue to cover your child. See above on my webpage and it even says so on USC’s webpage!

Our webpage on:

Special Needs Trusts

Mental Health Resources

SSI Supplemental Security Income

Medi Cal is automatic when you have SSI

Medi Cal & USC Coverage – Two policies?

how to set a Zoom Meeting

THE DUTY TO SUPPORT ADULT DISABLED CHILDREN

The Basics

California requires that the parents of adult children with incapacities support those children if possible. Family Code section 3910 states,

“The father and mother have an equal responsibility to maintain, to the extent of their ability, a child of whatever age, who is incapacitated from earning a living and without sufficient means.”

Incapacitated From Earning a Living

A child is incapacitated from earning a living if the child demonstrates “an inability to be self-supporting because of a mental or physical disability or proof of inability to find work because of factors beyond the child’s control.” Courts have been liberal in meeting this standard when dealing with the mental health of adult children and found the incapacity in the following cases to be sufficient.

In Chun v. Chun, a father was ordered to support an “emotionally disabled” adult child with a twelve-year-old maturity level.

In re Marriage of Drake dealt with a parent who was ordered to support an adult child with chronic paranoid schizophrenia.

Farber v. Olken involved an adult child who was mentally ill.

In order to demonstrate that an adult child has an incapacity sufficient for adult child support, an independent medical exam (IME) is required. In fact, for every adult child support case, an IME should be considered, even if the parties stipulate to the fact that the adult child is incapacitated. An IME will set a benchmark for the adult child, which will allow medical professionals to measure the extent of the adult child’s incapacity and the likelihood of the adult child developing a marketable skill set.

Without Sufficient Means

“[T]he question of ‘sufficient means’ should be resolved in terms of the likelihood a child will become a public charge.”

The principle that society should not bear the burden of caring for incapacitated adults who have parents with the means to do so. The “without sufficient means” inquiry concerns the issue of whether the adult child will end up requiring governmental benefits in the future.

It is also important to determine whether an adult child is already receiving such benefits.

See our resources & links below

In such a case, care should be taken to avoid the loss of such benefits through the use of a special needs trust or similar instrument. Nevertheless, some may argue that a proper adult child support order should eliminate any need for government benefits. However, certain benefits are frequently crucial to the health of the adult child and may be required as part of a medical regimen. For example, an adult child, who has an established course of treatment from a doctor that the adult child visited through the Social Security Administration, may need to remain on that course in order to avoid interruptions and complications that a change in medical provider would likely cause.

Also, the process to qualify for such benefits is fairly rigorous. A strong argument can be made that if an adult child has already qualified for government benefits, that adult child will likely qualify for adult child support. Read full article from Orange County Bar

Children Are Like Diamonds: Forever. Only, More Expensive: A Primer on California Family Code section 3910(a), the Most Terrifying, Most Common Sense Law You’ve Never Heard Of, but Should Have Read Article Alameda Bar Assoc.

Wallin & Klarich Family Law

Song Family Law

Proper standard for definition of incapacitated?

See Article on 50 year old attorney with depression

If my employer switches plans or I get a new job, will my disabled child be covered under the new plan?

We find that often policyholders are told that a new insurance company says that they will only cover disabled dependent children that are already enrolled on our group plan that happen to age out, not if you transfer plans, get a new job, etc.

Here is what we show the actual law and policy provisions to be:

If the employee or member changes carriers to another insurer or to a health care service plan, the new insurer or plan shall continue to provide coverage for the dependent child. CA Insurance Code 10277 (d)

This caused us to lose at least one new hire, because she decided to stay on her current medical plan (with her current employer) that provides coverage for her disabled adult child.

***I suggest you appoint us as your agent and we will fill out the disabled child form, along with the employee application and get a WRITTEN answer, not a “bozo” oral – hearsay (Federal Rules of Evidence) answer.

******

I currently work for a company that provides a group health plan. I have a disabled son age 27 covered on my policy.

I may be changing employer and going to a UC – University of California system.

How am I able to continue coverage for him through the UC system?

*************

Here’s the 2018 Health Benefits Guide for the UC System.

Page 6 Excerpt

If you are a newly hired employee with a disabled child over age 26 or if you acquire a disabled child over age 26 (through marriage, adoption or domestic partnership), you may also apply for coverage for that child. The child’s disability must have begun prior to the child turning age 26. Additionally, the child must have had continuous group health coverage since age 26, and you must apply for University coverage during your Period of Initial Eligibility. The plan will ask for proof of continued disability, but not more than once a year after the initial certification

See also Page 14

Question What about Self Insured Plans?

Answer

What does the evidence of coverage – EOC say? Please send your EOC to us or at least take a photo of your ID card with your Smart Phone and send to us. We don’t post individual identifiable information. We might then be able to search and find your EOC Evidence of Coverage and it would be so much easier to show you the benefits you have in your policy.

See above for more information

Would 10277 d apply if my disabled son is on his father’s plan, is now turning 26 and my X husband no longer wants our son on his Insurance?

Yes, we believe so. Your son has a special enrollment period to go onto your health insurance as he is losing minimum essential coverage.

Please send a copy of your evidence of coverage EOC or let us know the exact plan you have and we can see if we can find your EOC. EOC’s are mandated to be in Plain English.

My son’s father’s employer is refusing to drop our son from his health insurance they are saying we need a court order to take him OFF the insurance. Even though he is fully covered for state funded medi-cal as he is an SSI recipient.

My son has autism and his father’s insurance is denying recommended hours of treatment.

See our new webpage on Autism & Health Coverage

My sons father (ex-husband to be, legally we are still married) have been separated for 6 yrs I just never filed ,

He got a job and added our son to insurance

I found out because my son’s therapy was cxl [cancelled] because medical [medi-cal] said they are no longer the primary.

What can I do if I don’t want his dads work insurance since my son has medical [medi cal] and I’m his parent provider as well .

I feel this is a mess and I don’t even know where to start.

Please help?

Check our webpage on dual coverage Medi Cal & Employer Plans

Note also, that if you take your husband to court for child support or divorce, it’s quite likely the court will ORDER your husband to put the child on his employer coverage. Why should the tax payers provide coverage, when it’s available from an employer?

Sorry, but we are out of country on vacation…nor do we get compensated to help people with Medi Cal. If you have more questions, ask your Medi Cal HMO provider or see our contact page for Medi Cal.

my son, who is mentally disabled just turned 28

now united healthcare is trying to kick him off saying his disability occurred after he turned 18/19

even though they determined him to be disabled and allowed him to remain on the insurance after he turned 26.

Is he not grandfathered? Can they just chang the rules.

Check your evidence of coverage EOC

See “excerpt” of typical group plan above. It appears to me, it’s not if the disability was before or after age 18 or 19, but as long as it was before 26. See also the California Law in the very first section above. Age 26 shall not terminate coverage, if the child meets the criteria.

Also note, UHC can require proof of disability annually.

See the other FAQs for similar questions

My son is deaf and on my husband’s health insurance in sept he will be 26 can he stay on my husband’s insurance

Do you support him? Can he get a job? Can you get a doctors statement that he can’t work?

He can always get COBRA for 18 months if it’s an employer group plan.

Cal Cobra if a CA employer and you’re in CA for another 18 months

He can get ACA obamacare with no pre-existing clause. Click here for CA Quotes. http://www.quotit.net/eproIFP/webPages/infoEntry/InfoEntryZip.asp?license_no=0596610

Try these websites for help so that your son can find employment:

https://www.nad.org/

https://www.asha.org/public/hearing/Support-Services-for-Adults/

deaflinx.com

https://www.hearingloss.org/hearing-help/financial-assistance/

I’m disabled and on my Dad’s Group Health Plan. I am in the state of Virgnia. I have Medicaid as secondary insurance.

My father is retiring. When he loses his insurance policy, I am under the assumption that I will no longer be eligible for that insurance either.

He will start receiving Social Security, and I have been told at that point I will be eligible for Medicare. However, in my state people who are now on Medicare and Medicaid are being put into a new program called CCC+ It’s managed care. I am not sure if I will be able to continue seeing my current doctors on it or not.

Is there a retirement health plan for your Dad to stay on at his work?

If all else fails, there is COBRA for 18 months.

Medicare eligibility?

I don’t know about getting Medicare just because your Dad is getting Social Security. Were you on SSI? SSDI? Try these links:

https://socialsecurity.healthreformquotes.com/ssi/

medicare advocacy.org/medicare-coverage-for-people-with-disabilities/

If you find a citation showing that you can get Medicare based on your Dad getting Social Security, please post it!

Hi. Thank you for the links.

Because I was determined to be disabled before the age of 22, I will receive Social Security benefits not based on my work record but on one of my parents’ work record. Once a parent is eligible for benefits I receive 50% of their social security income as an SSDI benefit. If they were deceased, I would receive 75%.

The information is on the Social Security web-site:

Adults Disabled Before Age 22

An adult disabled before age 22 may be eligible for child’s benefits if a parent is deceased or starts receiving retirement or disability benefits. We consider this a “child’s” benefit because it is paid on a parent’s Social Security earnings record.

The “adult child”—including an adopted child, or, in some cases, a stepchild, grandchild, or step grandchild—must be unmarried, age 18 or older, have a disability that started before age 22, and meet the definition of disability for adults.

https://www.ssa.gov/planners/disability/qualify.html

In my case, because both of my parents have been working full time, I have been eligible for SSI based on my lack of resources and income and for Medicaid based on my disability and lack of income. Once my dad retires the situation changes in that I will receive SSDI. Some people in that case would also continue receiving SSI if the SSDI benefit was below a certain thresh-hold (based on how long the parent worked and earned). In my case I will just receive SSDI. I will also be eligible for Medicare. But because I will also still be in the income group eligible for Medicaid, I believe I will have the CCC Plus plan—although that is the part that the social worker wasn’t as sure about. It was being rolled out slowly, but she thinks now everyone may have to go on it.

I was able to find my private insurance policy I have now through my dad’s work and it looks like I could stay on but only if I paid the premiums which would be more than I will receive in SSDI. I did find a policy in Connecticut for the same insurance company where a disabled dependent can stay on one year without paying premiums after the policy ends for the employee, but that’s not the case in our state/plan.

Thank you for the provider search link for CCC Plus. It’s confusing because it seems more providers take Medicare or Medicaid than take one of the 6 managed care programs they’re putting CCC Plus people into. For example, I can see I would be able to continue seeing my PCP on some of the plans but not others, but I know he takes Medicare. And then I wonder if I’d be locked into that plan. I’m not sure how common acceptance of those CCC Plus plan is versus regular Medicare. I wonder if I’d be better off getting rid of Medicaid (if I’m allowed to even though I’m eligible) and paying for supplemental insurance for Medicare once I start receiving that. Something I will have to research more. But the provider search is a good start so I can check which of my current providers are covered by the 6 different plans.

Thank you again.

Do you get Medicare immediately or after two years?

I don’t know about opting out of CCC… I’m only licensed in CA. Here’s how to opt out of Cal Medi Connect

It’s one thing to simply not use Medi Cal, Medicaid, quite another to formally drop out of the program.

When you qualify for Medicare, that would make you eligible for Medi Gap, although the under 65 rates are higher than for a 65 year old.

You could also get a Medicare Advantage Plan

It’s confusing and complicated. I haven’t found many people that I could trust and are knowledgeable on all the rules…

I’m turning 26 in May my family has Cigna and I’m not sure what to do to stay on their insurance plan. I have fibromyalgia along with some other medical issues

Do you meet the definition of disabled above? That is, you can’t hold a job and are chiefly dependent on your parents for support?

Check with CIGNA’s member services, your Insurance Agent, your parents employer’s HR department and get the forms to certify (Sample from Oscar Insurance) your disability.

If you don’t meet the definition of disability, you can get special enrollment into ACA/Obamacare (get quotes) as you’ve lost coverage.

If you are not dependent on your parents… you may qualify for Medicaid either under MAGI Income Rules or aged & disabled. If you are getting SSI you automatically qualify for Medicaid.

I recently did a fundraiser for my friends disabled child and raised $13,000.

I need to know if I write a check for the proceeds to him, will he lose his coverage?

See our webpage above and review the definition of “chiefly dependent”

See also the IRS worksheet above

Please note the court ruled that there is no exact definition – so I can’t give you one

Hi,

I have a brother who is disabled by birth. My parents have passed away and I am now his legal guardian. Is there an age requirement (for my brother) on when I would become his legal guardian for him to qualify as a dependent on my health insurance?

Thanks

-Maggie

I don’t believe he would ever be your dependent for health insurance.

What about Medi Cal or Medicaid?

See dependent defintion here

and in a specimen policy here https://steveshorr.com/steveshorr/ab_1672_small_group_guaranteed_issue/Blue.Shield/2016/Eoc.platinum.201601PPO.pdf#page=71

WOW!!! you could be right!

3) A Dependent child is a child of, adopted by, or in legal guardianship of the Subscriber, spouse,

or Domestic Partner, and who is not covered as a Subscriber. A child includes any stepchild, child placed for adoption, or any other child for whom the Subscriber, spouse, or Domestic Partner has been appointed as a non-temporary legal guardian by a court of appropriate legal jurisdiction. A child is an individual less than 26 years of age (or less than 18 years of age if the child has been enrolled as a result of a court-ordered non-temporary legal guardianship.

A child does not include any children of a Dependent child (i.e., grandchildren of the Subscriber, spouse, or Domestic Partner), unless

the Subscriber, spouse, or Domestic Partner has adopted or is the legal guardian of the grandchild.

I’m not sure I fully understand your question… Please obtain the EOC evidence of coverage for your plan and we can double check everything.

How do we place our 27 year old daughter back on the Insurance to that it will pay for assisted living?

1st get the forms from your Insurance Company.

Verify that you qualify.

Is your daughter chiefly dependent upon you?

Will your coverage pay for assisted living?

Is that a medical treatment?

Is it in the Principal Benefits and Coverages (Covered Services) section of your coverage?

Is assisted living medically necessary?

Sample Evidence of Coverage

medical-necessity/

Does she need assisted living or Board & Care?

Does she have Medi Cal, Medicaid?

Medicare?

Is she on SSI?

Check these links:

assisted-living/

home-health-care-finding/

california-assisted-living-waiver/

long-term-care/

medi-cal-nursing-home/

https://socialsecurity.healthreformquotes.com/ssi/

aged-and-disabled-federal-poverty-level-program/

medi-cal-qualification-nursing-home/

My 30 year old son is autistic and continues to receive medical insurance coverage through my group health insurance plan (Healthnet) based on my retirement from the University of California.

He receives SSI and just received a Medicare Card in the mail that becomes effective on 1-1-19. The booklet accompanying the card is vague when it comes to deciding whether he should select or decline Medicare Part B. It states that he can sign up for Medicare part B through a Special Enrollment period at a later time without incurring a penalty as long as the family member is currently working.

Does the same rule also apply if the parent is retired and has group insurance coverage through the prior employer?

Thank you.

See our Medicare Part B page and Employer Plans

I did not know my son could stay on insurance, he was diagnosed while on the policy with schizophrenia, cannot work, it has been 2 years, can I get him back on the policy

Good Question. Does he qualify otherwise? Still chiefly dependent on you? Do you have Medi Cal, Medicaid? Dual Coverage?

Please send a copy of your evidence of coverage. See the sample EOC’s above, it looks like you have 24 months.

Did you get notification about your child being able to stay on the plan if you could show he was disabled?

(2) Chiefly dependent upon the employee or member for support and maintenance.

(b) The insurer shall notify the employee or member that the dependent child’s coverage will terminate upon attainment of the limiting age unless the employee or member submits proof of the criteria described in paragraphs (1) and (2) of subdivision

(a) to the insurer within 60 days of the date of receipt of the notification. The insurer shall send this notification to the employee or member at least 90 days prior to the date the child attains the limiting age. Upon receipt of a request by the employee or member for continued coverage of the child and proof of the criteria described in paragraphs (1) and (2) of subdivision (a), the insurer shall determine whether the dependent child meets that criteria before the child attains the limiting age. If the insurer fails to make the determination by that date, it shall continue coverage of the child pending its determination. https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=10277&lawCode=INS

Check the appeals procedures in your EOC

My son used to be on my health insurance via my employer and was removed when he turned 26 yrs old, he is now 29 and disabled.

Would I be able to put him back on my health insurance with my employer and have Medicaid as a secondary insurance for him?

I am in the state of Kansas.

I doubt it as he wasn’t disabled before age 26. Please read the law cited above 3 times and when you think you understand it, read it again. If you have more questions, put them here.

ACA/Obamacare is guaranteed issue. You can have an individual policy in addition to Medicaid – Medi-Cal (California)

In CA, you can get quotes here.

It wouldn’t hurt to fill out the forms to ask, but I don’t see that your employers health plan is mandated to take it. I only do CA and National Health Laws, if Kansas has something that might help you, you would have to check with the Department of Insurance there or see if you can find a top notch agent there. Here’s the NAHU Agent Finder.

My daughter will be 26 in April 12, 2020. She was diagnosed with bipolar 1, etc etc October 2019. and is totally dependent on us since August 2019.

Our insurance carrier, is refusing to allow her to stay on my insurance past age 26 because she wasn’t dependent on us in 2019 and 2018.

Their premise is that if she wasn’t dependent on our taxes she is not eligible. She wasn’t disabled till very recently and before age 26.

Please advise me on how to proceed?

We can’t give you legal advice, but we can point out policy provisions, reference materials and the appeals process through State of CA and what it shows in your Evidence of Coverage.

How about reviewing the guide to contract interpretation above.

Please send a copy of your evidence of coverage and the disability forms you sent to the Insurance Company and their replies.

This is what looks like the relevant portion of Insurance Code 10277

I don’t see any requirement that the child has to be disabled for any period of time before age 26, just before age 26.

With so recent a diagnosis, maybe they don’t believe she is truly dependent?

For reference, check out the rules to be considered disabled for Social Security

Check this page about SSI Supplemental Security Benefits, there are attorneys there…

Check this page on Medi Cal

When anyone loses coverage, they are guaranteed issue special enrollment into an Individual Plan, get quotes.

Check the appeal provisions in your evidence of coverage.

My son is 26 and disabled and lives with us. We do not claim him as a dependent on our tax return.

The insurance is now asking for a copy of our tax return.

Will that be a problem?

How will you show that your child is chiefly dependent on you and your husband?

We are no longer able to do complex research pro bono. We now charge for tutoring, education and research.

You might try these links to find help to show your child is chiefly dependent on you.

I have a 26+ year old child deemed incapable of self support and receiving social security disability. I just started a new job and have been told she is NOT eligible for health care coverage.

xxx healthcare is claiming they only have to extend coverage to those children who were in their insurance plans prior to age 26 regardless of my being a new employee.

Do you mean the Insurance Company is saying they won’t transfer the benefit over, from your prior employer, when you say:

who were in their insurance plans

Has your child been on your prior coverage?

Insurance Code 10277 d

(d) If the employee or member changes carriers to another insurer or to a health care service plan, the new insurer or plan shall continue to provide coverage for the dependent child.

The new plan or insurer may request information about the dependent child initially and not more frequently than annually thereafter to determine if the child continues to satisfy the criteria

Would 10277 d apply if my disabled son is on his father’s plan, is now turning 26 and my X husband no longer wants our son on his Insurance?

Yes, we believe so. Your son has a special enrollment period to go onto your health insurance as he is losing minimum essential coverage.

Please send a copy of your evidence of coverage EOC or let us know the exact plan you have and we can see if we can find your EOC. EOC’s are mandated to be in Plain English.

My son has had SSDI for 2 years and now has Medicare. He may also qualify for Medi-Cal (Medicaid)

Would having Government or other coverage disqualify him from remaining on an individual or employer group plan from his parents?

I don’t see anything in the law (which we can only point out to you, we are not attorney’s and can’t interpret or advise you) or Sample EOC – Evidence of Coverage that says that he would not qualify for having other coverage.

Just review our pages on dual coverage…

What if disabled child lives with father, and pays majority of support, but medical insurance is paid by mother through employer.

Child will be 26 next March.

Each parent meets only one requirement.

Can child still be covered by mother after age 26?

I believe so. Both of you are still the parents. The child is still dependent on his/her parent (s)

I’m out of country. If you haven’t resolved this with your employer’s insurance company, email me mid May

What happens if a disabled dependent over 26 gets married? Does the parents’ coverage for that person end?

I can’t seem to find an answer to this. (California resident).

Good question. Is the disabled person still “chiefly dependent” on the policy holder, see above? If you do lose coverage, that would give you a special enrollment into ACA – get quotes here.

What Insurance Company are we talking about? I can then pull the forms and proofs for that specific company.

While this page is very popular 189 hits in the last 30 days, no one is buying Insurance from me and thus I haven’t kept up posting the revised forms. I’m happy to when asked.

Yes, she is “chiefly dependent” on her parents’ insurance for lifelong medical care.

The policy holder is Anthem Blue Shield/blue Cross.

She also received SSI benefits.

Please read again, at least 3 times, what chiefly dependent means. It doesn’t mean how much she needs or uses the insurance, but if her parents are supporting & maintenance for her. Please review the footnotes above that I’ve just added.

Now that she’s married, is her husband supporting and providing maintenance for her?

If she has SSI that provides around $1,000/month for support. Are her parents providing more than that? In addition, SSI automatically gives her Medi-Cal coverage.

In CA telling me Blue Cross – Blue Shield means nothing. They are two separate companies.

Please send a copy of her ID card. Then I will know and can get further details. I will not post any PHI – Protected Health Information. If I do post the ID card, I will blot that out.

Thanks for the ID card. The plan your friend has is not one that I’m an authorized agent for. Please have her or her parents log into their “member portal” and then you can review the actual EOC full policy and the forms that BC/BS requires to prove disability. Also you can check the definition of dependent and from what I can tell in general, being married doesn’t disqualify a child. I’m concerned about “chiefly dependent.” Please review the page above again, as I just updated it.

My son was diagnosed with Autism and sensory integration disorder when he was 8 years old.

I applied for disability and he was denied.

He is now 25 and will lose his insurance (our plan) BCBS in April of 2023.

How should I proceed?

He isn’t officially disabled.

Here’s more information on our website about Autism and here

What kind of disability are you talking about?

SSI? SSDI? Medi Cal?

How do you know your son will lose the group coverage? Did you apply? Does he meet the requirements in your EOC Evidence of Coverage?

I don’t see anywhere, where it requires that one be “officially? disabled to continue the parents plan. Have you given your doctor the official insurance forms to fill out?

If you don’t get Medi Cal or stay on the group plan, your son can get an Individual ACA Guaranteed Issue Plan. Get quotes

See also COBRA and Cal COBRA

We appied for SSDI.

He does meet all of the requirements; [to stay on the group health plan] with one exception. Documentation of severity from his current primary.

This is my quandry. His current primary is asking for instruction on this documentation and our insurance doesn’t provide instruction or documents/forms.

Simply put, his primary doesn’t know him. He has given him a yearly physical exam for 5 years. The front office recieved a copy all diagnoses during the transition from his pediatrician so I have not accompanied him into the exam. I couldn’t make my request more simple. I haven’t approached BCBS regarding the hesitancy of his current primary to document and submit a letter of severity out of fear they may question our integrity.

In my experience, having written diagnoses from multiple doctor’s and therapists does not equate to having a ‘disabled status’ when sourcing advocacy. I have struggled to find resources time and time again because he does not carry a legal status. I am fortunate that my son is strong and continues to learn and compensate for his disability but I am truly petrified at the thought of not having medical care for him

As far as getting information from your doctor… It’s beyond my pay grade.

Please ask your Insurance Company for a Copy of the Evidence of Coverage! It probably says that a form will be provided. Try asking your doctor to fill out another Insurance Companies form.

The closest information I have would be Social Securities Manual above

Here’s the section on Evidence 614

Here’s our webpage on appeals & grievances

Here’s some attorney’s that might be able to help you.

Has your son worked & held a job? Are you applying for SSI or SSDI? If SSI Medi Cal is automatic!

See above about ACA/Obamacare.

How about buying this book from Nolo?

Great information.

I will try another company’s insurance forms.

Unfortunately, this plan [my current health insurance] wouldn’t have evidence (ongoing therapies) before 2017. He had medicaid and batch blues (bcbs) prior to 2017.

He has never had a job or wanted to drive. He attends community college and has almost completed an associates in fine arts. He doesn’t drive and has never had a physical relationship to my knowledge. I was a young mother (22) and made the decision that I would facilitate his growth and make accommodations as they arose. This may or may not have been the right decision. I am confident I made the most informed decisions with the help of TEACCH [Autism Program]; who administered his final evaluation. They provided a diagnosis along with invaluable resources. Like TEACCH, your research and advice have given me much of the same. The difference at this crossroad is the absence of youthful optimism. Your support, guidance and generosity have allowed me to objectively hope for great things. My appreciation is incredibly complex, articulating proper words is beyond reach. Your work is completely profound. I hope you understand the impact you have made in my life. Please, please please continue this work- specifically for the silent dreamers that just can’t give up.

Thank you always.

Great idea! Thank you!

My daughter became disabled and unable to support herself at age 27.

She had already been terminated from my company plan (a CA plan) at age 26.

Might there be any possible way I can get her back on my CA Employer Coverage?

Near as I can tell, the law lets coverage end at age 26. Here’s clarification in Blue Shield’s Group plan

A Dependent child who reaches age 26 becomes ineligible on the day before his or her 26th birthday, unless the Dependent child is disabled and qualifies for continued coverage as described in the definition of Dependent.

I don’t see a way to get her on your bosses coverage. She wasn’t disabled prior to age 26.

How about an Individual Plan? Free Quotes

Cal or COBRA?

SSI?

Medi-Cal

SSDI

Medicare?

Doesn’t the obama care plan (Covered CA) depend on your income?

I have a niece (>27yo) who is also low income and without a job and covered CA only allowed her to get a medi-Cal policy.

We are hoping for fewer exclusions and more coverage choices

ACA – Obama Care – Covered CA only asks for your income if you want subsidies, tax credits to pay for your premiums. If you use our quote engine, you can get quotes both with and without subsidies.

Here’s the income chart to see what enhanced silver level you might get, Medi-Cal, subsidies, etc. Again, if you don’t want subsidies, don’t ask for them. No one can force you to take Medi-Cal.

Here’s what I have on the benefits for Medi-Cal. I don’t get paid to do Medi-Cal. If you find something about benefits that I don’t have, please post it to help your fellow website visitors.

All new insurance plans, must have these 10 essential benefits. ACA wanted to standardize shopping around for plans, so the only real choices are doctor lists, metal levels and insurance company service – reputation.

Do we have a special enrollment period for your daughter to get coverage now? Otherwise we have to wait till 11.1.2017 for Open Enrollment to get a plan for 1.1.2018.